Exhibit 99.1

Operator: Greetings and welcome to the MAXIMUS 2014, second quarter conference call. At this time all participants are in a listen-only mode. A question-and-answer session will follow the formal presentation.

If anyone should require operator assistance during the conference, please press star-zero on your telephone keypad. As a reminder, this conference is being recorded.

I would now like to turn the conference over to your host, Lisa Miles, Senior Vice President of Investor Relations for MAXIMUS. Thank you. You may now begin.

Ms. Lisa Miles: Good morning.

Thank you for joining us on today’s conference call. I would like to point out that we’ve posted a presentation on our Web site under the Investor Relations page to assist you in following along with the call.

With me today is Rich Montoni, Chief Executive Officer; David Walker, Chief Financial Officer, and Bruce Caswell, President and General Manager of the Health Services Segment.

Before we begin, I’d like to remind everyone that a number of statements being made today will be forward-looking in nature. Please remember that such statements are only predictions, and actual events and results may differ materially as a result of risks we face, including those discussed in Exhibit 99.1 of our SEC filings.

We encourage you to review the summary of these risks in our most recent 10-K filed with the SEC. The company does not assume any obligation to revise or update these forward-looking statements to reflect subsequent events or circumstances.

Today’s presentation may contain non-GAAP financial information. Management uses this information in its internal analysis of results and believes that this information may be informative to investors in gauging the quality of our financial performance, identifying trends in our results and providing meaningful period-to-period comparisons. For a reconciliation of non-GAAP measures presented in this document, please see the company’s most recent quarterly earnings press release.

05/08/14 - 9:00 a.m. ET - 1

And with that, I’ll turn the call over to Dave.

Mr. David Walker: Thanks, Lisa.

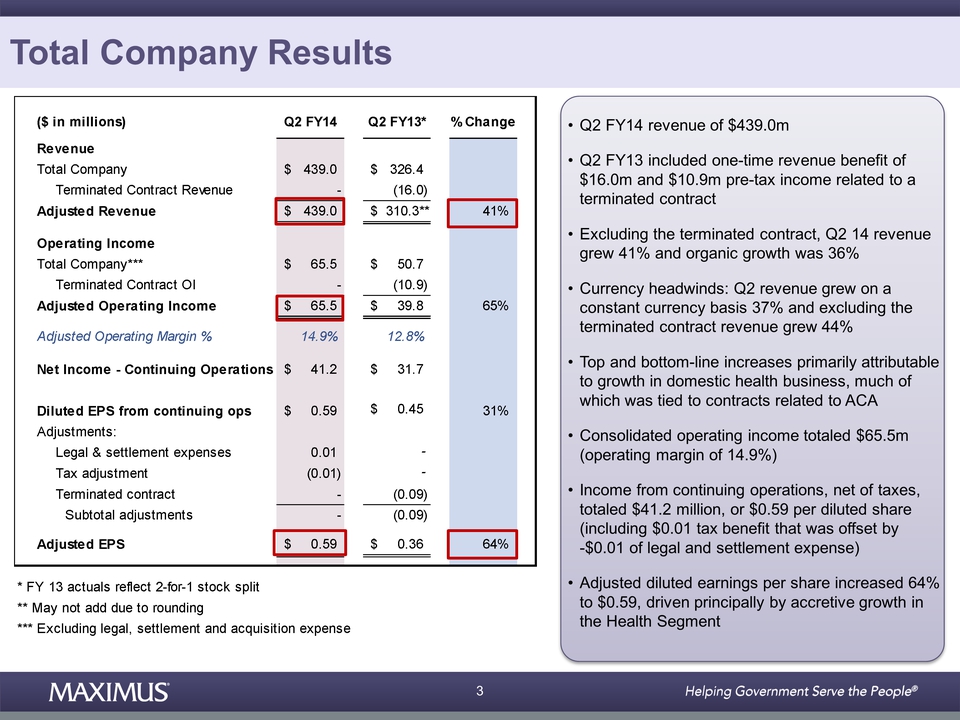

This morning MAXIMUS reported second quarter revenue of 439 million dollars. This compares to 326.4 million dollars reported for the same period last year. As a reminder, last year’s second quarter results included the effect of a one-time revenue benefit of 16 million dollars and 10.9 million dollars in pretax income related to the termination of a contract acquired with PSI in 2012.

The nature of this termination is such that it is unlikely to be repeated and does not reflect the underlying nature of the business. Accordingly, as in prior years, we will provide comparatives that exclude the effect of this contract termination. Our press release includes reconciliations from our GAAP results to non-GAAP numbers, showing our results excluding this contract.

On a GAAP basis, revenue increased 35 percent compared to the same period last year, and organic growth was 30 percent. Excluding the 16 million dollars of revenue from the terminated contract, second quarter revenue grew 41 percent compared to the same period last year, and organic growth was 36 percent.

We experienced some currency headwinds in the quarter, and as a result on a constant currency basis, revenue growth would have been better at 37 percent or 44 percent excluding the terminated contract.

05/08/14 - 9:00 a.m. ET - 2

Top and bottom line increases for the quarter were attributable primarily to the growth in our domestic health business, much of which was tied to contracts related to the Affordable Care Act.

As expected consolidated operating income was strong and totaled 65.5 million dollars in the second fiscal quarter and operating margin was 14.9 percent.

For the second quarter, income from continuing operations net of taxes increased to 41.2 million dollars or 59 cents per diluted share. This included a one cent tax benefit that was offset by one cent of legal and settlement expense.

Normalizing for these items, adjusted diluted earnings per share increased 64 percent to 59 cents in the second quarter of fiscal 2014, driven principally by accretive growth in the health segment. This compares to 36 cents of adjusted diluted earnings per share, which excludes approximately nine cents related to the terminated contract that we reported for the same period last year.

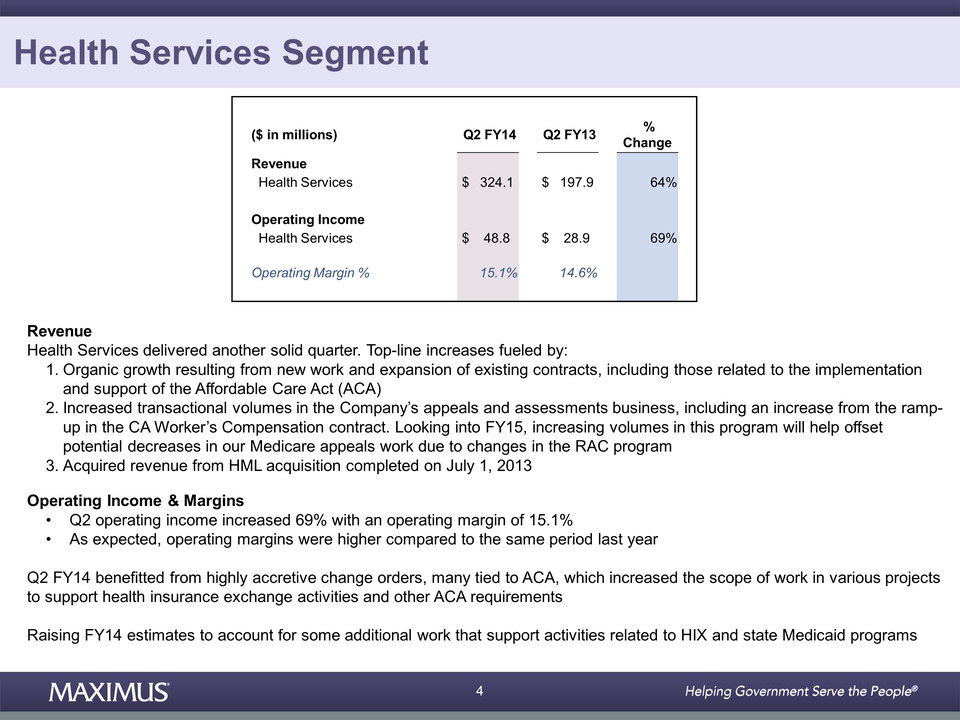

Let’s jump into results by segment, starting with Health Services. As expected, the Health Services Segment delivered another solid quarter with revenue increasing 64 percent to 324.1 million dollars, compared to the same period last year.

Year-over-year top line increases were fueled by three things. One, organic growth resulting from new work and expansion of existing contracts, most notably those related to the implementation and support of the Affordable Care Act.

Two, increased transactional volumes in the company’s appeals and assessment business, including the year-over-year increases from the ramp-up in the California Workers Compensation contract, which we expect will continue through fiscal 2014.

05/08/14 - 9:00 a.m. ET - 3

Looking into fiscal 2015, the increasing volumes on this program will help offset potential decreases in our Medicare appeals work due to changes in the RAC program, and lastly, required revenue from the HML acquisition that we completed on July 1 of last year.

Health Services Segment operating income in the second quarter of fiscal 2014 increased 69 percent compared to the same period last year and totaled 48.8 million dollars with an operating margin of 15.1 percent. As expected, operating margins for the Health Services Segment were higher compared to the same period last year and driven by accretive growth.

As we mentioned on our last call, the segment’s second quarter benefited from a handful of highly accretive change orders, many of which were tied to the Affordable Care Act. These change orders increased our scope of work in various projects to support health insurance exchange activities and other ACA requirements.

As noted in this morning's release, we are also raising our 2014 full year estimates to account for some additional work that supports various activities related to the health insurance exchanges and state Medicaid programs.

The fact that our clients continue to turn to MAXIMUS during times of significant need is a testament to the value add we bring, a proven track record to get the job done and the strength of our brand.

We remain a trusted partner to our government clients, and we believe our experience in providing exceptional support through the first open enrolment period bodes well for future opportunities over the next three to five years as other states consider long-term options for operating their own health insurance exchanges. All in all, another great delivery from the health services team.

05/08/14 - 9:00 a.m. ET - 4

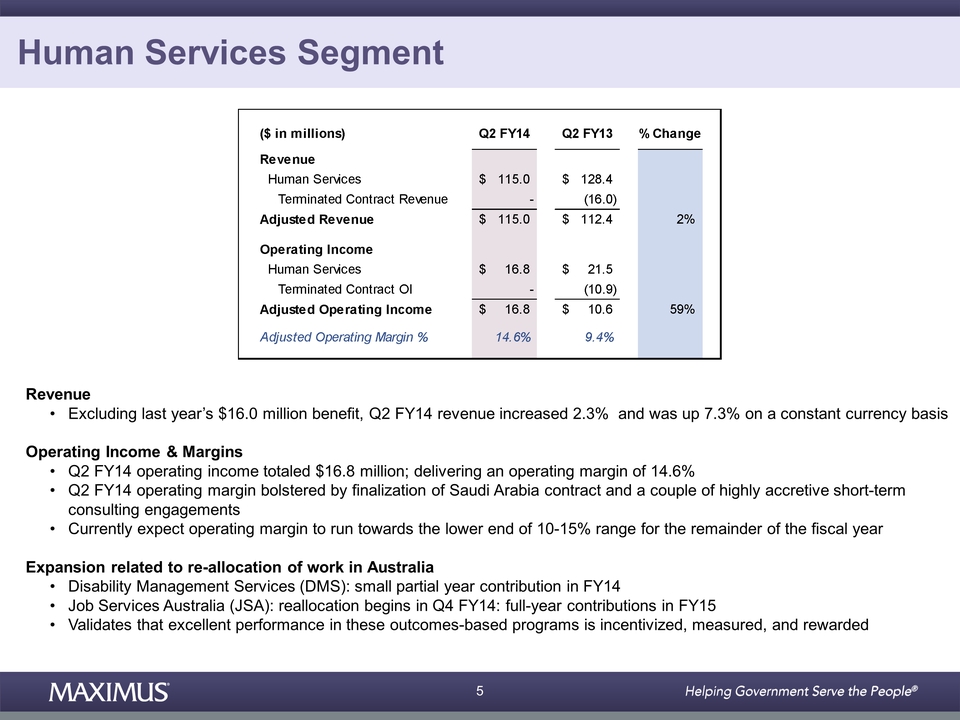

Now let's turn our attention to financial results for Human Services. For the second fiscal quarter, revenue for the Human Services Segment totaled 115 million dollars.

This compares to 128.4 million dollars for the same period last year, which included a 16 million dollars benefit to revenue from the terminated contract. Excluding this benefit, revenue in the second quarter of fiscal 2014 increased 2.3 percent and was up 7.3 percent on a constant currency basis compared to last year.

Second quarter operating income for the Human Services Segment totaled 16.8 million dollars, which compares favorably to the prior year of 10.6 million dollars, after normalizing out the pre-tax benefit from the terminated contract.

The operating margin in the second quarter of fiscal 2014 was stronger at 14.6 percent, bolstered by the finalization of our contract in Saudi Arabia and a couple of highly accretive, short term consulting engagements in the U.S.

As we mentioned last call, we currently expect operating margins for the Human Services Segment to be running towards the lower end of our 10 to 15 percent range for the remainder of fiscal 2014.

We also have some very good news to share out of Australia, where we were notified on an expansion related to reallocation of work in two of our Australian contracts, Disability Management Services, or DMS, and Job Services Australia, known as JSA.

05/08/14 - 9:00 a.m. ET - 5

Rich will provide additional details about these expansions. But from a financial perspective we will see a small, partial year contribution at fiscal 2014 for DMS. The additional work from our larger contract, JSA, is not expected to begin until Q4 of fiscal 2014, and we expect both will provide full year contributions in fiscal 2015.

Overall, this is great news and further validates that our excellent performance in these outcome-based programs are incentivized, measured and rewarded under Australia’s star ratings program.

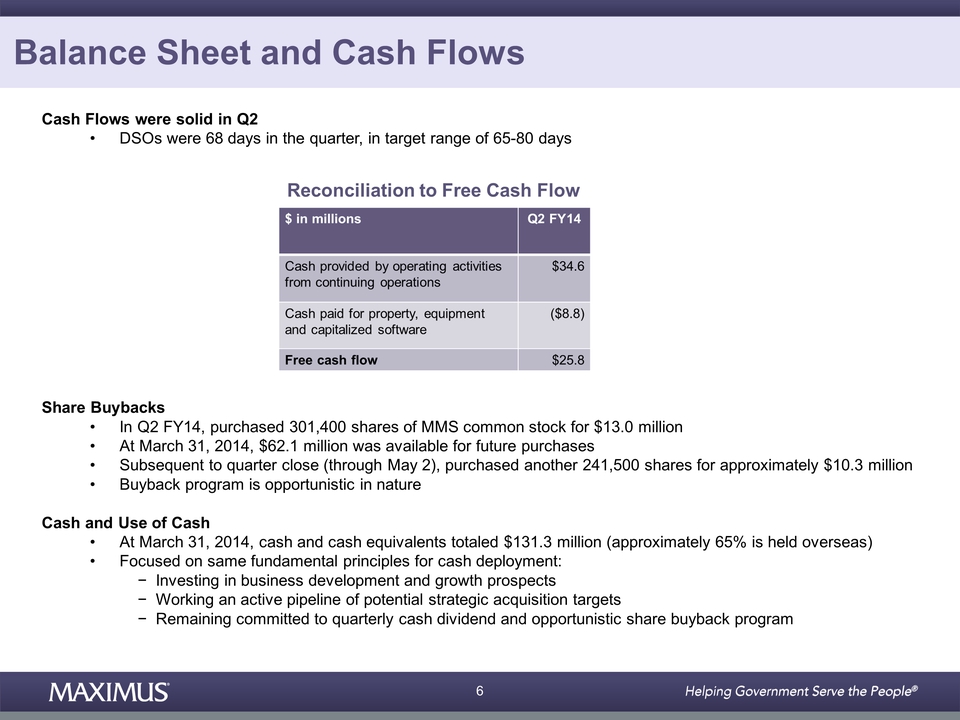

Moving on to cash flow and balance sheet items, cash flow was again solid in the quarter. DSO’s were 68, well within our target range of 65 to 80 days.

For the second quarter of fiscal 2014, cash provided by operating activities from continuing operations totaled 34.6 million dollars, and free cash flow was 25.8 million dollars. As a reminder, free cash flow is defined as cash provided from operating activities from continuing operations, plus property and equipment and capitalized software.

During the quarter we purchased 301,400 shares of MAXIMUS common stock for approximately 13 million dollars under our Board authorized program. At March 31st, we had approximately 62.1 million dollars available for future repurchases. Subsequent to quarter close through May 2nd, we purchased another 241,500 shares for a total of 10.3 million dollars.

As we’ve said in the past, we consider our buyback program to be opportunistic in nature, and the recent purchases reflect our overall value that we see to the purchasing of our own shares.

At March 31st, we had 131.3 million dollars in cash and cash equivalents, of which approximately 65 percent is held overseas. We remain focused on the same fundamental principles for cash deployment, which include investing in business development and growth prospects across our markets. This includes both organic and strategic acquisitions.

05/08/14 - 9:00 a.m. ET - 6

We continue to work an active pipeline with potential targets, but we are highly selective and tend to run a very rigorous process. Therefore, the process takes time. We also remain committed to our quarterly cash dividend and opportunistic share buyback program.

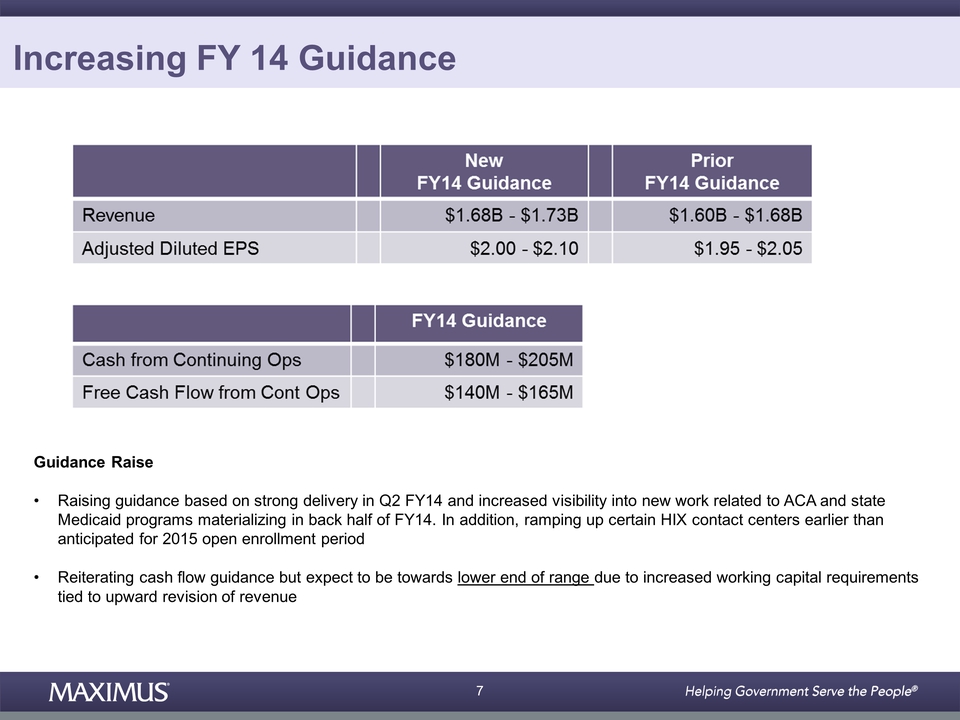

And lastly, guidance, as I mentioned earlier, we are increasing our fiscal 2014 revenue and earnings guidance. We now expect revenue in fiscal 2014 to range between 1.68 billion and 1.73 billion dollars, and we expect earnings per diluted share from continuing operations to range between two dollars and two dollars and 10 cents.

We are raising our guidance based on a strong delivery in the second quarter and increased visibility into additional work related to the Affordable Care Act and State Medicaid Programs in the back half of the year.

We previously expected a decrease in work and revenue in the second half of fiscal 2014, following the completion of the first open enrolment period. However, we have a handful of contracts where our clients are leveraging our customer contact staff to meet other urgent needs.

In addition, we are already working with our clients on the staffing models for the upcoming open enrollment period in the fall. Much of our work will start ramping up in the summer in preparation for this open enrollment period.

In certain customer contact centers, we’ve already been directed to increase our planned staffing levels and scope of work, which also had a direct benefit on our fiscal 2014 estimates.

05/08/14 - 9:00 a.m. ET - 7

We are very pleased to be provided with these additional opportunities in helping our clients manage considerable change. We are reiterating our cash flow guidance for fiscal 2014, but now expect to be towards the lower end of the range due to increased working capital requirements tied to the upward revision or revenue.

Thanks for joining us this morning, and now I’ll turn the call over to Rich.

Mr. Richard Montoni: Good morning and thank you, David.

Our solid results in the quarter reflect our success in responding to our clients' needs, especially during the first year of such a high profile reform effort as the Affordable Care Act.

As a trusted partner to governments, we see many opportunities to provide them with innovative, flexible, and scalable ways to reform their social programs. However, it often takes years for these new programs to move forward, from concept to launch, to a normalized steady state.

What we are seeing payout today are the long-term growth strategies from MAXIMUS. As a reminder, these include enhancing our U.S. operations by supporting clients through the next phase of the Affordable Care Act, expanding our international operations through health and human services opportunities in multiple geographies, and growing our federal business as evidence by several years of robust growth in this business line.

I’d like to walk you through each of these drivers and provide you updates and details on how they continue to server as growth platforms. Let's start off with our U.S. operations and the largest growth driver to fiscal ’14, supporting our clients’ efforts to meet the requirements under ACA.

05/08/14 - 9:00 a.m. ET - 8

We mentioned on last quarters call that our clients faced some significant technology challenges during the first open enrolment period. In response, MAXIMUS provided enhanced consumer assistance through our customer contact centers.

In many cases, we helped consumers complete applications over the phone in order to finish the enrolment processes. This led to a high spike in volumes in many of our HIX contact centers. In fact, our customer service representatives across all or our centers handled a total of approximately five million calls from October through March.

We were able to react to the volume increases quickly. Our operational model is scalable and we are able to leverage existing overflow capabilities in other contact centers and rapidly add incremental capacity.

Our ability to provide response and solutions our clients has continued after the conclusion of the first open enrollment period. We’ve been pleasantly surprised with the resiliency of demand. As expected, call volumes have come down, but as David noted, we’ve added some supplemental work related to ACA and Medicaid.

In addition, we are also ramping up some of our contact center operations at higher levels than originally expected, in preparation for the next open enrolment period. The result is a backfill of revenue that has largely led to the increase to our fiscal ’14 estimates.

Over the longer term, we are preparing for the best way to support our clients with the ongoing implementation and stabilization of the Affordable Care Act. As we mentioned before, this is a multiyear growth driver for MAXIMUS, as steady state enrolment and the exchanges is not expected until 2017 to 2018.

05/08/14 - 9:00 a.m. ET - 9

Over time, as was the case with Medicaid, other states will likely adopt state-based exchanges to have more control over coverage expansion, access to federal funds for marketing and outreach, and to maintain a closer linkage to state insurance regulations. Medicaid expansion and other Medicaid support services are also part of our long-term growth strategy under ACA.

Some states, including New York and California, are already using ACA-related funding to expand their Medicaid programs. These expansions include new service areas, such as Royal Counties, where provider networks can now support managed care, and additional populations like the dual eligibles.

We are proud to be working closely with several state clients who are participating in demonstration programs with the centers for Medicare and Medicaid services, to provide coordinated care to dual eligibles.

Other states are exploring alternative mechanisms to expansion, including waivers to use federal funds in new ways such as premium assistance and healthy incentive programs.

All waiver requests must be approved by the CMS. So, while we are supporting early states in this model, we anticipate that this will remain a longer-term growth driver for MAXIMUS.

Let's move on to our international operations where we have several irons in the fire to drive long-term growth. We are excited to be expanding our footprint in Australia through the service area reallocations that David noted earlier. Let's start with the reallocation for our Disability Management Services or DMS program.

05/08/14 - 9:00 a.m. ET - 10

Under this program, we provide case management services to individuals with injuries, disabilities, or other major health issues. The DMS reallocation shifted employment service areas from underperforming vendors to those with demonstrated success. MAXIMUS increased its overall disability employment business share with an additional 12 service areas, bringing our total number of DMS areas to 32.

From a revenue perspective, it adds about 5 million dollars in new annual revenue, and when fully ramped, this contact should contribute about 22 million dollars annually. This is an important confirmation that solid execution leads to increased market share under these performance based contracts.

The Australian government also recently announced that effective June 23rd, 2014, there will be reallocations under the Job Services Australia program which is known as JSA.

JSA is our largest welfare to work program, where we currently service a caseload of approximately 75,000 job seekers. Our performance is measured through the achievement of sustainable employment outcomes, which the government reports publicly each quarter through their star rating program.

While the government hasn’t finalized all the details of the reallocations, they indicated some JSA vendors will be replaced by higher performing vendors. Our performance to-date remains consistently strong and we received verbal notification that we will receive some reallocated work.

Presently, this contact runs at about 125 million dollars annually and we are hopeful that this increased market share could provide between 10 and 15 percent of new annual revenue and increase our caseload to more than 100,000.

05/08/14 - 9:00 a.m. ET - 11

We believe these additional awards will also support MAXIMUS is the next rebid of the JSA contract. We currently expect the request for tenders to drop towards the end of this calendar year, and keep in mind that there are two important aspects of this type of rebid.

First, the Australian government historically has placed greater reliance on performance than price for these types of contracts. Second, it’s not an all or nothing bid, because the awards are based on site locations. Given our past performance, we remain cautiously optimistic as we continue in our role as a significant trusted partner to the Australian government.

In the U.K., the Department for Work and Pensions recently published quarterly work programs statistics that cover the performance period up to December 31st, 2013. As a prime provider, MAXIMUS has helped approximately 11,000 individuals into a job that they have held for more than six months or in some cases three to six months.

These statistics also show that MAXIMUS achieved targets for a significant percentage of the payment groups within the program. In fact, we were third among 18 providers for the overall cumulative percentage of referrals for which we received a job outcomes payment.

Overall, performance for all work program providers has remained stable. The Department for Work and Pensions is currently working on its first inter-region reallocation, where high performing vendors can bid to pick up an entirely new region.

Under this particular allocation, MAXIMUS is eligible to bid on a region, and we are reviewing the opportunity. However, our interest is predicated on the terms and conditions of how the government intends to transition the region from one vendor to another. This is a new process for the U.K. government, and we will keep a close eye on the opportunity.

05/08/14 - 9:00 a.m. ET - 12

That said, it's also important to recognize that we don’t expect reallocation under the work program to be the primary growth driver in the U.K. for MAXIMUS in the near term, rather we remain very excited about the other emerging opportunities in the U.K., where we established a foothold in the health services market, with last year’s acquisition of Health Management.

We continue to focus on several larger, near term opportunities, where we can leverage Health Management’s position as the largest occupational healthcare provider, and build upon our established reputation with the U.K. government. We are actively preparing bids and feel positive about these prospects, but we are not far enough along in the process to provide any more details at this time.

Wrapping up our long-term growth discussion with a third area, expanding our federal book of business, we made good progress with introducing our core capabilities to new federal programs and agencies.

During the quarter we came to a successful resolution on the protest under our new debt management contract with the U.S. Department of Education, to help administer a portfolio of defaulted student loans. We are currently ramping up. Our operations remain on track to launch in August.

This new contract is a prime example of our efforts to extend our core offerings such as citizen engagement, customer contact centers and case management to a wider set of federal agencies.

Our federal team has also successfully launched our eligibility appeals operation for the federal marketplace. We’ve been able to help consumers whose applications were previously incomplete to reapply and complete in the enrollment process.

05/08/14 - 9:00 a.m. ET - 13

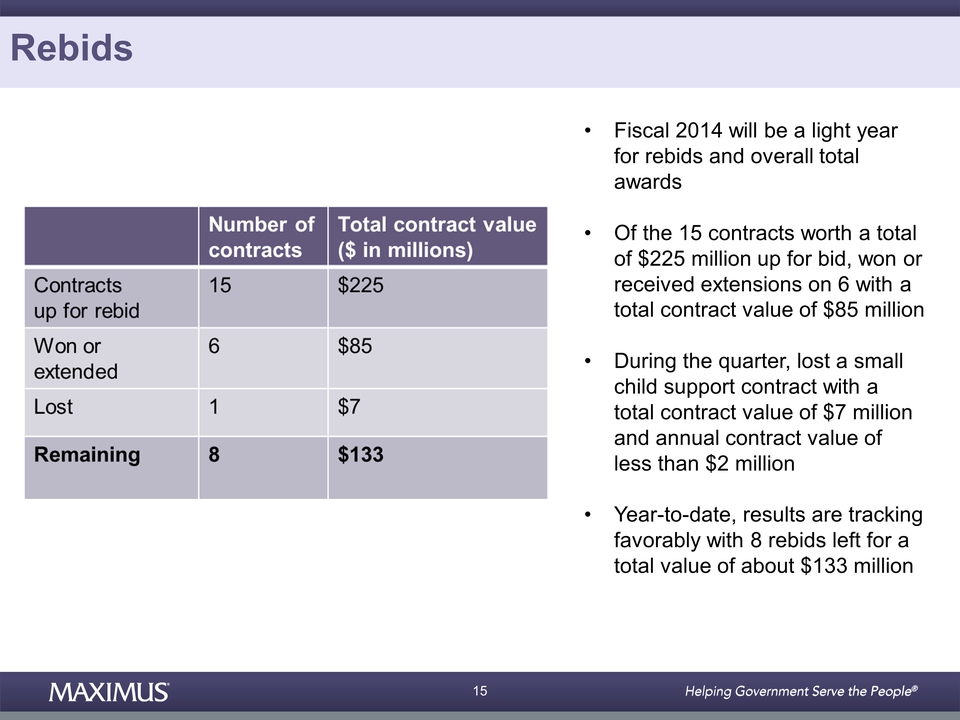

Moving onto rebids, on previous calls we mentioned that fiscal 2014 will be a light year for rebids and hence overall total awards. Of the 15 contracts with a total contract value of 225 million dollars up for rebid, we’ve won or received extensions on six, with a total contract value of 85 million dollars.

During the quarter, we lost a small child support contract, with a total contract value of approximately 7 million dollars and an annual contract value of less than 2 million dollars. So, year-to-date, results are tracking favorably. We have eight rebids left for a total value of about 133 million dollars.

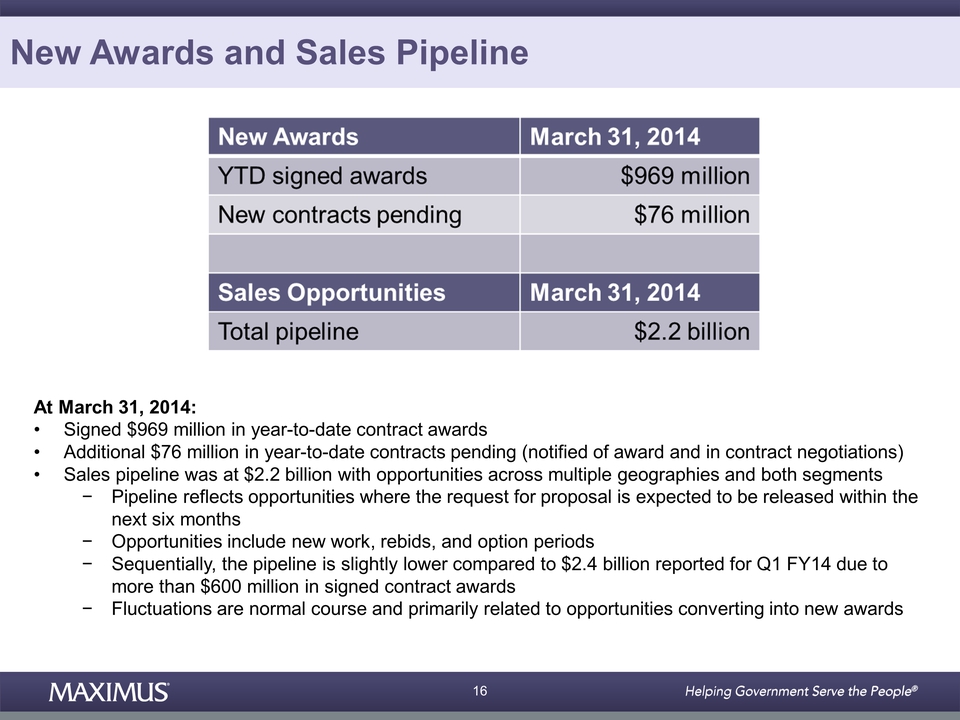

Wrapping up with our new sales awards in the pipeline, for the second quarter of fiscal 2014, year-to-date signed awards were 969 million dollars. At March 31st, 2014, we had an additional 76 million dollars in new contracts pending, where we’ve been notified of the award and are under contract negotiations.

This compares to 425 million dollars in contracts pending last year, which included approximately 390 million dollars from two large program rebids and extensions.

Our sales pipeline at March 31st, 2014, remains steady at 2.2 billion and includes opportunities across multiple geographies in both segments. As a reminder, our pipeline only reflects opportunities where the request for proposal was expected to be released within the next six months. These opportunities include new work, rebids, and option periods.

This is consistent with last year’s total pipeline of 2.3 billion. On a sequential basis, the pipeline is slightly lower compared to the 2.4 billion reported for the first quarter of fiscal 2014, due to more than 600 million in signed contract awards. These fluctuations are a normal course for our pipeline and are primarily related to opportunities converting into new awards.

05/08/14 - 9:00 a.m. ET - 14

In closing, we are very pleased with our results this quarter, an improved outlook for the full fiscal year of 2014. And as we look beyond fiscal 2014, all eyes are on the many opportunities ahead for MAXIMUS and how fiscal 2015 is shaping out.

We are at the start of our annual planning process and plan to give you additional insights as factors develop on our next quarterly call, as well as formal guidance on our end of year call in November.

As we’ve said all along, the underpinnings of our growth are driven by long-term demand trends tied to operating large government social programs. The overarching demand tails are decades long in nature and driven by demographic shifts and pressured government budgets.

While program or legislative changes often create specific opportunities for MAXIMUS, it's important to note that the timing of these opportunities can vary.

We’ve consistently said that in the long term we believe we can grow revenue and earnings by 10 percent. There will be years of accelerated growth where we are above the 10 percent mark, like fiscal years ’13 and ’14, and there will be years where our overall growth may be tempered by start-ups, rebids, or government procurement cycles.

So, what does all this mean for fiscal 2015? There are many dynamics in play, including meaningful new business opportunities that ultimately will drive the formal guidance we issue for 2015.

05/08/14 - 9:00 a.m. ET - 15

But based on what we see today, we expect fiscal 2015 to be a good growth year. Ultimately, we manage a total portfolio of contracts. So just like any other year, fiscal 2015 will have its own headwinds and tailwinds that will shape our outlook.

First, we mentioned MAXIMUS benefited from additional ACA and Medicaid related work that helped bolster fiscal 2014. Based on our experience with operating other health programs, we believe some of this additional work will continue and some will abate.

In addition, we see seasonality of our HIX contracts, but it's too early to predict precisely how next year’s open enrollment spike will compare to this year.

On the new business side, our pipeline remains robust with several key opportunities that could materialize in fiscal 2015 and boost growth. There’s a lot of backfill in motion and a handful of large bids that are in process.

We are diligently working these opportunities that are right in our sweet spot, and we remain optimistic on our overall prospects for success.

Overall, we see our year-to-date performance and expectations for the remainder of fiscal 2014 as additional confirmation of the long-term growth opportunities for MAXIMUS in fiscal 2015 and beyond.

So, we look forward to keeping you further informed as to specific growth expectations for fiscal 2015, as we progress through our planning process, and as these pending new opportunities evolve.

We remain excited to continue to provide our clients and program beneficiaries the highest quality of service. We appreciate all the great efforts our employees put forth daily, and we thank you for your continued interest and support.

05/08/14 - 9:00 a.m. ET - 16

And now, let's open it up for questions. Operator?

Operator: Thank you.

At this time, we'll be conducting a question and answer session. If you would like to ask a question, please press star-one on your telephone keypad. A confirmation tone will indicate your line is in question queue.

You may press star-two if you would like to remove your question from the queue. For participants using speaker equipment, it may be necessary to pick up your handset before pressing the star keys.

In the interest of time, please limit your questions to one question and one follow up question. And then you may come back into queue for further questions. One moment please while we poll for questions.

Our first question comes from Charlie Strauzer from CJS Securities.

Mr. Charlie Strauzer: Hi. Good morning.

Mr. Richard Montoni: Good morning, Charlie. How are you?

Mr. Charlie Strauzer: Good.

I was hoping, Richard or David, you know if you could give us a little bit more color on how we should think about the breakdown between quarters and the guidance from both a segment perspective and a margin perspective, to help us kind of you know plan out the models. This is--there’s a shift that sounds like a little bit more on the back half.

Mr. Richard Montoni: Okay. All right, Charlie.

We'd be glad to do that. I’m going to ask Dave Walker to take the lead on it.

05/08/14 - 9:00 a.m. ET - 17

Mr. David Walker: Hi Charlie.

You know from a consolidated perspective, we have additional work coming through that uplifts our guidance for the year as you know, and compared to the second quarter, the third quarter may be seasonally lower, and the fourth quarter may come on a bit stronger.

And this is due to some of the larger HIX contact centers winding down after the first open enrollment and then ramping back up for the next open enrollment period. In addition, historically, we’ve seen seasonality in the fourth quarter at the end of the government fiscal.

In Human Services, our guidance for Human Services remains unchanged. You know however, we’ve had some currency headwinds, which mostly impact Human Services.

So, we expect revenue for the remainder of the year to be fairly consistent with Q2. And we still expect that operating margin for the remainder of the year will run towards the lower half of our 10 to 15 percent range.

In Health, our guidance rate is principally driven by health segment, and this work is expected to come in a bit stronger in Q4 as we prepare for the next open enrollment period. So, overall, we still expect that that segment would deliver full year operating margin towards the higher end of our 10 to 15 percent range.

Mr. Charlie Strauzer: Great.

And then, Rich maybe you can talk a little bit more about JobPath, Ireland. I know that’s a relatively new opportunity for you.

Mr. Richard Montoni: Glad to do that, Charlie.

05/08/14 - 9:00 a.m. ET - 18

And there’s a number of opportunities that we have out there and over in the European geography. I’m not going to get into any particular one that’s in progress.

But there are a number of countries as we’ve talked about over the years that we think will be right for opportunities. And you know we’ll sort through them, we’ll submit proposals where it's appropriate, and keep our fingers crossed that we’ll be successful.

Mr. Charlie Strauzer: Great. Thank you very much.

Ms. Lisa Miles: Next question please.

Operator: Our next question comes from Carl McDonald from Citigroup.

Mr. Carl McDonald: Great. Thank you.

I had a question on the Australia rebid. Point well taken on them preferring the performance measures over price. I think you’ve also talked about the Australia contract being above the high end of the margin target range. So, is it right to think about it as part of a rebid process that margins probably would come back more towards the target level?

Mr. Richard Montoni: Carl, I think that’s a fair question. And generally, you know we see performance-based contracts towards the higher end of the range, and in a rebid environment it's always possible that government will come back and change the terms, the conditions, the pay points that give you some adjustment.

But in my mind, I haven’t really put this one on the table as one where I expect there's always degree of uncertainty. I have not felt that this is one where we’d expect a dramatic change in margins.

Mr. Carl McDonald: Okay.

05/08/14 - 9:00 a.m. ET - 19

And then just on the timing of that, if the if the rebid comes out at the end of this year, the projected timeline for when that new contract would start?

Mr. Richard Montoni: That would be for July 1, 2015, in terms of a handover if that happens.

Mr. Carl McDonald: Got it. Thank you very much.

Mr. Richard Montoni: You bet.

Ms. Lisa Miles: Next question please.

Operator: Our next question comes from Dave Styblo from Jefferies.

Mr. Dave Styblo: Good morning.

Thanks for taking the questions, guys. Staying on the Australia topic here, could you help us understand a little bit more of the additional work that you won? It sounds like some of the DMS revenue is going to fall on this year, but most of the JSA would happen next year. Can you maybe quantify the impact that that’s having on guidance for this year?

Mr. David Walker: It doesn’t impact it greatly. And it's included in the guidance this year.

Mr. Dave Styblo: Okay.

Mr. David Walker: And it has a much more dramatic impact next year obviously.

Mr. Dave Styblo: Okay.

And then the--I guess before I had thought the government’s approach and frequency of reallocating work would happen more around the rebid. So, is there an opportunity for you guys to win even more as they go through a rebid? Or was this reallocation something about a one-off event that they decided to do at this time?

05/08/14 - 9:00 a.m. ET - 20

Mr. David Walker: We don’t view it as a one-off event. I think it's pretty much a recurring element of their process. And they're quite proud of it. And I think it’s a good feature. They do a quarterly star ratings program. And they use that as a driver to reallocate work. And I think it’s a very important mechanism for them to drive best value in the program.

So, in sum, I don’t think it is a one-off type situation. And I had not thought of it as something tied closely to the rebid situation.

And interestingly enough, when you think it through, given that methodology it almost sets up a rebid situation where you--all things considered equal, there’s likely to be less turnover during a rebid than other types of models.

Mr. Dave Styblo: Okay.

And if I could ask my follow-up on the appeals, I know the last quarter you talked about the RAC appeals and some of the volumes easing for next year.

You knew you had line of sight for this year for stabilization. But the offsets to that, you had mentioned the California Workers Comp. I’m curious, is the margin profile on that business similar to perhaps the decline that you may observe in RAC?

Mr. David Walker: The margin on those businesses is very comparable. So in fact the margin backfills quite nicely for any downturn we may see in other areas.

And it really does manage like a portfolio. You know some are up. Some are down with very similar margin features. It tends to be transaction-based and run you know on a very careful basis across the U.S.

Mr. Dave Styblo: Okay. Thanks.

05/08/14 - 9:00 a.m. ET - 21

Mr. Richard Montoni: You bet. Thank you.

Ms. Lisa Miles: Next question please.

Operator: Our next question comes from Brian Kinstlinger from Sidoti & Co.

Mr. Brian Kinstlinger: Great. Thanks. Good morning, guys.

Mr. Richard Montoni: Good morning, Brian.

Brian Kinstlinger: In your results to date can you confirm you haven’t received meaningful revenue from appeals? I know you--I think you said the DOE also is launching in August. And then when do you expect these two programs to be in a serious ramp?

Ms. Lisa Miles: Brian, I just want to ask you a clarifying question. Do you mean the eligibility appeals tied to the federal marketplace contract?

Mr. Brian Kinstlinger: That’s right. Thank you.

Ms. Lisa Miles: Okay.

Mr. David Walker: You know, Brian, that contract is ramping up nicely. And it’s running as consistent with our expectations.

Mr. Richard Montoni: And the DOE contract as you know is early stages--.

Mr. Brian Kinstlinger: --Yep--.

Mr. Richard Montoni: And as well as ramping up. And I think the handoff's effective, is scheduled to be effective August timeframe.

Mr. David Walker: August. Yeah, fourth quarter.

Mr. Richard Montoni: So, then I think the key takeaway is there are very early ramp stages moving forward according to our plan. And obviously given they are early start ups, we watch them very, very closely.

05/08/14 - 9:00 a.m. ET - 22

Mr. David Walker: Yeah. DOE will not be material this year. Yeah.

Mr. Brian Kinstliner: And in Australia, the volumes that you're expecting on caseloads are up 33 percent, 75,000 to 100,000, yet you only expect 10 to 15 percent more revenue. Maybe you can talk about the disconnect between those two numbers.

Mr. Richard Montoni: Sure. I’ll be glad to do that.

I think that the major factor--and keep in mind, these are very, very early estimates. And we still have to sit down with the client and negotiate the particulars, so all that’s subject to change.

But that being said, these early estimates, the difference really is a function of mix and as you know you get paid different--meaningfully different pay points for different types of cases that we handle. So the difference would really be in the mix category.

Mr. Brian Kinstliner: Thank you.

Mr. Richard Montoni: Sure.

Ms. Lisa Miles: Next question please.

Operator: Thank you.

Once again, if you do have a question, please press star-one at this time. Our next question comes from Richard Close from Avondale Partners.

Mr. Richard Close: Yes.

Thank you, for allowing me to ask the questions. With respect to the long-term growth, you highlighted the 10 percent. And then you commented ’15's expected to be a good growth year.

So, is a good growth year somewhere between the 10 percent and what we’re achieving in the current fiscal year?

05/08/14 - 9:00 a.m. ET - 23

Mr. Richard Montoni: I think that’s a great question, Richard. And my sense on this is, again, it's really too early to put a percentage or even a range, if you will, on what does that good growth year mean.

I don’t think it’s a simple yes or no answer. And I think it’s too early to handicap because we’ve got so many pieces that are moving.

I think, a good growth year in my mind is a growth year that supports our long term, not meaning single year 10 percent metric, but our long term view that we can grow our business 10 percent. And if we have confirming evidence in any year that that’s a very reasonable expectation, then I put that in the good category.

Mr. Richard Close: With respect to the pending new opportunities or I think that your talking in terms of long term you know growth in ’15 and beyond, you know as you think about you know those opportunities, as you sit here today and obviously you guys give us a six-month pipeline, and you can see things out farther than that.

You know are you I guess as pleased with the opportunities you know today as we were a year ago? Or how do you, you know, see the overall business? Is it improving or is it you know normalizing?

Mr. Richard Montoni: I think that’s a good question as well, Richard. I this, that again I think long term. I think the nature of our business model, the nature of our industry, is that it’s a multiyear process to generate growth, long term growth.

And given the long term nature of some of these opportunities that can take several years to go from thought to final contract, we really do have to look at things over a long-term period. And that’s why we always refer to the long term growth drivers that we think are decades long in nature.

05/08/14 - 9:00 a.m. ET - 24

And I do think that you’ll have years, and certainly this year is one of those years, where we have a hyper growth rate. You know given30 percent plus type growth rates, those don’t sustain forever.

I think clearly this year we’ve benefited from perhaps the most significant piece of legislation in the United States history in these social programs. And we've been--we’ve had a front row seat in that regard. So, the Affordable Care Act will not repeat in fiscal ’15. So, we’ll see some abatement.

That being said, I’m very pleased to see that there are other programs in health and human services, not only in the U.S., but in other countries that are stepping up in carrying us forward into future years.

Whether all of that adds up to be you know 15 percent plus in fiscal ‘15 or not I think is one metric. But I also look at how does it shape up in years beyond ’15, and again, I fall back to that long-term 10 percent plus growth rate.

Mr. Richard Close: All right. Thank you very much.

Mr. Richard Montoni: You’re welcome.

Ms. Lisa Miles: Next question please.

Operator: Our next question comes from Frank Sparacino from First Analysis.

Mr. Frank Sparacino: Hi guys.

I was just wondering if you could maybe give some additional color on Medicaid expansion particularly. I’m not sure if there’s any way to quantify what the impact has been thus far, but you know also more curious, just relative to your expectations, you--how you see that this year and next year.

Mr. Richard Montoni: Okay. Good morning, Frank.

05/08/14 - 9:00 a.m. ET - 25

Also with us here is Bruce Caswell. And I think most of you know Bruce. Bruce is the General Manager and President of our Health Segment. And we are going to ask Bruce to talk a little bit about that.

Mr. Bruce Caswell: Sure. And good morning, Frank.

It’s a great question. One way to address this is to really look at it at a top level from the enrollment numbers that have come out recently. And when you look at the sources, overall about 13.5 million, newly eligible individuals have been determined eligible to enroll.

And that breaks out into about 8.7 million who are ABTC or tax credit eligible, of which the numbers suggest that about 8 million of them have already paid, selected their plan and paid their premium.

The remainder is new Medicaid CHIP lives. So, that’s about 6.7 million nationally. Of which about 2.25 million are attributable to woodwork effects. So, these are individuals that would have previously eligible under program rules who because of the outreach efforts of the program obviously came into Medicaid.

So, if you net the 2.25 from the 6.7, I think you get actually at an aggregate scale the Medicaid expansion effect. And there is some data that’s been published out there that breaks that out by state, obviously with the 25 states that are participating Medicaid expansion and those that are not.

Our view has been and continues to be that Medicaid expansion is a long-term trend. It--there will be states that over time will expand Medicaid because of obviously the pressures related to the loss of disproportionate share payments to the hospitals.

We’ve seen pressurization during the state legislative season. Just this year it remains the number one issue, for example, as Virginia tries to get to a budget.

05/08/14 - 9:00 a.m. ET - 26

In addition to that, CMS has very much indicated flexibility to states that seek waivers to expand Medicaid on their own terms.

And a core element of that is doing an expansion that has a component of personal responsibility, whether it's financial participation, something as simple as a two-dollar co-pay every time you go see a physician, to some element of personal responsibility and engaging in active and healthy lifestyle behavior.

So we see states now that are crafting expansion programs. Arkansas was kind of the poster child for this originally, but there are a number of others. Pennsylvania, Michigan, and others that are looking at doing expansion on their terms, and we feel that we are in an excellent position as an incumbent providers with existing infrastructures.

With this, it goes back several years. We said we’ve got programs and technology that can be, if you will, pivoted to support those expansion initiatives. So, we feel very strongly about our position in assisting those states as this in a multiyear basis continues to roll out.

Next question please.

Operator: Thank you.

As a final reminder, if you do have question, please press star-one at this time. Our next question is a follow up from Brian Kinstlinger from Sidoti & Co.

Mr. Brian Kinstliner: Great. Thanks.

In the U.K. work program, you said you were eligible to bid and that vendors can pick any new region. I’m curious, is every vendor that’s there able--eligible to bid?

Or did you have to meet certain standards? And can you only add one new region? Is that what you meant to say?

05/08/14 - 9:00 a.m. ET - 27

Mr. Richard Montoni: I think that’s what we meant to say, Brian. I don’t believe that all vendors are eligible, but the government does have certain criteria in order for vendors to be eligible to bid.

I don’t know how many of the vendors are eligible, but it’s a subset of all of them. And I believe there’s one region that we are particularly interested in.

Ms. Lisa Miles: That’s correct.

Brian it goes back to the original framework and what vendors were allowed to bid in that specific region, when they did the initial work program bidding.

And so, I am more than happy to circle back with you. But the statistics are also on the department for Work and Pensions website in terms of what vendors are eligible to bid on the specific region.

Mr. Brian Kinstlinger: Great. That’s helpful.

And then the last question, I was surprised that gross margin in Health Services was higher in the June quarter versus the March quarter given the higher mix of cost plus work I assume from the federal programs that you are running related to ACA. So, can you go over may be, Dave, the puts and the takes for this line item.

Ms. Lisa Miles: Do you mean the March quarter versus the December quarter?

Mr. Brian Kinstlinger: Yeah. I do.

Ms. Lisa Miles: Okay.

Mr. Brian Kinstlinger: That’s the second time you had to correct me. Thank you. I do.

Mr. Richard Montoni: Why don’t you just repeat the question for the other folks on the call, David?

05/08/14 - 9:00 a.m. ET - 28

Mr. David Walker: Yeah.

I mean the question is surprise about the high margins essentially this quarter on a sequential basis.

Mr. Richard Montoni: For Health.

Mr. David Walker: For Health. Right.

And we talked about the size of the change orders in the call that happened in Q2. And those were primary in Health. So, we just look at the ACA and Medicaid related change orders for work performed prior to this quarter, you know in which we got the change order portion this quarter. So, it's highly accretive. It's 5.2 million dollars.

You know we’re about four, four and a half cents a share, which falls right to the bottom line. And you know when we talk about Duals and Medicaid expansion, that’s a lot--that's what lot of this work is.

So, we've been seeing expansion of Medicaid. We’ve been seeing Duals and other mandates under the Affordable Care Act. So again, there is a lot of change out there. And that’s opportunity for us.

Mr. Brian Kinstlinger: Thank you.

Ms. Lisa Miles: Next question please.

Operator: Thank you.

At this time we have no further questions. I would like to thank our participants for joining. You may now disconnect.

05/08/14 - 9:00 a.m. ET - 29

Fiscal 2014 Second Quarter Earnings David N. Walker Chief Financial Officer and Treasurer May 8, 2014

Forward-looking Statements & Non-GAAP Information These slides should be read in conjunction with the Company’s most recent quarterly earnings press release, along with listening to or reading a transcript of the comments of Company management from the Company’s most recent quarterly earnings conference call. This document may contain non-GAAP financial information. Management uses this information in its internal analysis of results and believes that this information may be informative to investors in gauging the quality of our financial performance, identifying trends in our results, and providing meaningful period-to-period comparisons. These measures should be used in conjunction with, rather than instead of, their comparable GAAP measures. For a reconciliation of non-GAAP measures to the comparable GAAP measures presented in this document, see the Company’s most recent quarterly earnings press release. A number of statements being made today will be forward-looking in nature. Such statements are only predictions and actual events or results may differ materially as a result of risks we face, including those discussed in our SEC filings. We encourage you to review the summary of these risks in Exhibit 99.1 to our most recent Form 10-K filed with the SEC. The Company does not assume any obligation to revise or update these forward-looking statements to reflect subsequent events or circumstances. 2

Total Company Results Q2 FY14 revenue of $439.0m Q2 FY13 included one-time revenue benefit of $16.0m and $10.9m pre-tax income related to a terminated contract Excluding the terminated contract, Q2 14 revenue grew 41% and organic growth was 36% Currency headwinds: Q2 revenue grew on a constant currency basis 37% and excluding the terminated contract revenue grew 44% Top and bottom-line increases primarily attributable to growth in domestic health business, much of which was tied to contracts related to ACA Consolidated operating income totaled $65.5m (operating margin of 14.9%) Income from continuing operations, net of taxes, totaled $41.2 million, or $0.59 per diluted share (including $0.01 tax benefit that was offset by -$0.01 of legal and settlement expense) Adjusted diluted earnings per share increased 64% to $0.59, driven principally by accretive growth in the Health Segment 3

Health Services Segment Revenue Health Services delivered another solid quarter. Top-line increases fueled by: 1. Organic growth resulting from new work and expansion of existing contracts, including those related to the implementation and support of the Affordable Care Act (ACA) 2. Increased transactional volumes in the Company’s appeals and assessments business, including an increase from the rampup in the CA Worker’s Compensation contract. Looking into FY15, increasing volumes in this program will help offset potential decreases in our Medicare appeals work due to changes in the RAC program 3. Acquired revenue from HML acquisition completed on July 1, 2013 Operating Income & Margins Q2 operating income increased 69% with an operating margin of 15.1% As expected, operating margins were higher compared to the same period last year Q2 FY14 benefitted from highly accretive change orders, many tied to ACA, which increased the scope of work in various projects to support health insurance exchange activities and other ACA requirements Raising FY14 estimates to account for some additional work that support activities related to HIX and state Medicaid programs 4

Human Services Segment Revenue Excluding last year’s $16.0 million benefit, Q2 FY14 revenue increased 2.3% and was up 7.3% on a constant currency basis Operating Income & Margins Q2 FY14 operating income totaled $16.8 million; delivering an operating margin of 14.6% Q2 FY14 operating margin bolstered by finalization of Saudi Arabia contract and a couple of highly accretive short-term consulting engagements Currently expect operating margin to run towards the lower end of 10-15% range for the remainder of the fiscal year Expansion related to re-allocation of work in Australia Disability Management Services (DMS): small partial year contribution in FY14 Job Services Australia (JSA): reallocation begins in Q4 FY14: full-year contributions in FY15 Validates that excellent performance in these outcomes-based programs is incentivized, measured, and rewarded 5

Balance Sheet and Cash Flows Cash Flows were solid in Q2 DSOs were 68 days in the quarter, in target range of 65-80 days Share Buybacks In Q2 FY14, purchased 301,400 shares of MMS common stock for $13.0 million At March 31, 2014, $62.1 million was available for future purchases Subsequent to quarter close (through May 2), purchased another 241,500 shares for approximately $10.3 million Buyback program is opportunistic in nature Cash and Use of Cash At March 31, 2014, cash and cash equivalents totaled $131.3 million (approximately 65% is held overseas) Focused on same fundamental principles for cash deployment: − Investing in business development and growth prospects − Working an active pipeline of potential strategic acquisition targets − Remaining committed to quarterly cash dividend and opportunistic share buyback program 6

Increasing FY 14 Guidance Guidance Raise Raising guidance based on strong delivery in Q2 FY14 and increased visibility into new work related to ACA and state Medicaid programs materializing in back half of FY14. In addition, ramping up certain HIX contact centers earlier than anticipated for 2015 open enrollment period • Reiterating cash flow guidance but expect to be towards lower end of range due to increased working capital requirements tied to upward revision of revenue 8

Fiscal 2014 Second Quarter Earnings Richard A. Montoni President and Chief Executive Officer May 8, 2014

Responding to the Needs of Our Clients Solid results in second quarter reflect our success during first year of the Affordable Care Act (ACA) Continued success is based on seeking innovative, flexible and scalable ways to reform social programs Takes years for new programs to move from concept to launch to normalized steady-state Long term growth strategies for MAXIMUS: − Enhancing U.S. operations by supporting clients through next phase of ACA − Expanding international operations through health and human services opportunities in multiple geographies − Growing federal business line 9

U.S. Operations and ACA Update Supporting our clients’ efforts to meet the requirements under ACA and to respond to technology challenges during the first open enrollment period − Provided enhanced consumer assistance through our contact centers – in many cases, helped consumers complete applications over the phone to finish the enrollment process − Handled a total of approximately five million calls from October through March − Reacted to the volume increases quickly, leveraging overflow capabilities in other contact centers and rapidly adding incremental capacity Providing responsive solutions for our clients after the conclusion of the first open enrollment period − Surprised with the resiliency of demand − Despite call volumes coming down, added supplemental work related to ACA and Medicaid − Ramping up certain contact center operations at higher levels than originally expected in preparation for the next open enrollment period − Resulting in a back-fill of revenue that has largely led to increase our FY14 estimates Preparing for the best way to support our clients with ongoing implementation and stabilization of ACA − Multi-year growth driver, as steady-state enrollment in the exchanges is not expected until 2017 to 2018 − Over time, other states will likely adopt state-based exchanges to have more control over coverage expansion, access to federal funds for marketing and outreach, and to maintain a closer linkage to state insurance regulations 10

Medicaid Expansion and Other Support Services Medicaid expansion and other Medicaid support services are also part of our long-term growth strategy under ACA Some states already using ACA-related funding to expand Medicaid programs Expansions include new service areas and additional populations like the dual eligibles Proud to be working with several clients participating in the Centers for Medicare & Medicaid Services (CMS) demonstration programs to provide coordinated care to dual eligibles Other states are exploring alternative mechanisms to expansion, including: − Waivers to use federal funds in new ways − Premium assistance and healthy incentive programs All waiver requests must be approved by CMS, so while we are supporting early states in this model, we anticipate that this will remain a longer-term growth driver 11

International: Australia Update Expanding our footprint in Australia through service area reallocations Disability Management Services (DMS) – Provide case management services to individuals with injuries, disabilities or other major health issues DMS reallocation shifted service areas from under-performing vendors to those with demonstrated success We increased our overall disability employment business share with an additional 12 employment service areas, bringing our total DMS areas to 32 Adds $5 million in new annual revenue and when fully ramped should contribute $22 million annually Confirmation that solid execution leads to increased market share under these performance-based contracts Job Services Australia program (JSA) – Largest W2W program; we serve approximately 75,000 job seekers Performance is measured through the achievement of sustainable employment outcomes Government reports publically each quarter through their Star Rating program Some JSA vendors will be replaced by higher performing vendors − Notification that we will receive some reallocated work − Current contract runs about $125 million annually and this increased market share could provide: Between 10% and 15% of new annual revenue Increased caseload to more than 100,000 Additional awards will also support next rebid of the JSA contract and currently expect request for tenders to drop towards the end of this calendar year. Two important aspects of this type of rebid: − Australian government historically has placed greater reliance on performance than price for these types of contracts − Not an “all or nothing” bid because the awards are based on site locations Remain cautiously optimistic in our role as a trusted partner to Australian government 12

International: United Kingdom Update The Department for Work and Pensions (DWP) recently published quarterly Work Programme statistics that cover the performance period up to December 31, 2013. As a prime provider, MAXIMUS: − Helped approximately 11,000 individuals into a job that they have held for more than six months (or in some cases three to six months) − Achieved targets for a significant percentage of the payment groups within the program − Was third among all 18 providers for the overall cumulative percentage of referrals for which we have received a job outcomes payment Relative performance for all Work Programme providers has remained stable DWP working on first inter-region reallocation where high-performing vendors can bid to pick up a new region − We are eligible to bid on the region and are reviewing the opportunity − Our interest predicated on terms and conditions of transitioning the region to new vendor − A new process for the UK government we will keep a close eye on the opportunity − Work Programme reallocations not expected to be primary UK growth driver in the near term Rather, remain excited about other emerging opportunities in the UK − Established a foothold in the health services market with last year’s acquisition of Health Management, the largest occupational health care provider − Continue to focus on several larger near-term opportunities − Build upon established reputation with the UK government − Actively preparing bids and feel positive about these prospects 13

Expanding Federal Book of Business Good progress on introducing our core capabilities to new programs and agencies U.S. Department of Education (DOE) − Successful resolution on protest − Help administer a portfolio of defaulted student loans − Ramping up operations and remain on track to launch in August DOE contract is a prime example of extending our core offerings to a wider set of federal agencies − Citizen engagement − Customer contact centers − Case management Successfully launched eligibility appeals operations for Federal Marketplace − Help consumers whose applications were previously incomplete, to reapply and complete enrollment process 14

Rebids Fiscal 2014 will be a light year for rebids and overall total awards Of the 15 contracts worth a total of $225 million up for bid, won or received extensions on 6 with a total contract value of $85 million During the quarter, lost a small child support contract with a total contract value of $7 million and annual contract value of less than $2 million Year-to-date, results are tracking favorably with 8 rebids left for a total value of about $133 million 15

New Awards and Sales Pipeline At March 31, 2014: Signed $969 million in year-to-date contract awards Additional $76 million in year-to-date contracts pending (notified of award and in contract negotiations) Sales pipeline was at $2.2 billion with opportunities across multiple geographies and both segments − Pipeline reflects opportunities where the request for proposal is expected to be released within the next six months − Opportunities include new work, rebids, and option periods − Sequentially, the pipeline is slightly lower compared to $2.4 billion reported for Q1 FY14 due to more than $600 million in signed contract awards − Fluctuations are normal course and primarily related to opportunities converting into new awards 16

Opportunities Ahead Shape Fiscal 2015 At the start of our annual planning process and plan to give: − Additional insights on next quarterly call − Formal guidance on end-of year call in November Underpinnings of growth driven by long-term demand trends tied to operating large government social programs Overarching demand tails are decades-long in nature and driven by: − Demographic shifts − Pressured government budgets While program or legislative changes often create specific opportunities; timing of these opportunities can vary Long-term, believe we can grow revenue and earnings by 10% − Some years will have accelerated growth above the 10% mark (FY13 and FY14) − Other years may have overall growth tempered by start-ups, rebids or government procurement cycles 17

What Does This Mean for FY15? Meaningful new business opportunities that will ultimately drive our guidance for FY15 − Expect good growth year with its own headwinds and tailwinds Additional ACA- and Medicaid-related work that helped bolster fiscal 2014 − Some additional work will continue and some will abate − Seasonality in HIX contracts, too early to predict next year's open enrollment spike will compare to this year Pipeline remains robust with several key opportunities that could materialize and boost growth − Handful of large bids that are in process and right in our sweet spot − Remain optimistic on our overall prospects for success 18

Conclusion Year-to-date performance and expectations for the remainder of FY14 as additional confirmation of long-term growth opportunities in FY15 and beyond Look forward to reporting specific growth expectations for FY15 as we progress through our planning process and as the pending new opportunities evolve Remain excited to continue to provide our clients and program beneficiaries the highest quality of services Appreciate all the great efforts by our employees Thank you for your continued interest and support 19