Exhibit 99.2

MAXIMUS Fiscal 2013 Third Quarter Conference Call

Earnings

Call Transcript

Operator: Greetings, and welcome to the Maximus Fiscal 2013 Third Quarter Conference Call.

At this time, all participants are in a listen only mode.

A brief question and answer session will follow the formal presentation.

If anyone should require operator assistance during the conference, please press star, zero on your telephone keypad.

As a reminder, this conference is being recorded.

It is now my pleasure to introduce your host, Lisa Miles, Senior Vice President of Investor Relations for Maximus.

Thank you, Ms. Miles. You may begin.

Ms. Lisa Miles: Good morning. Thank you for joining us on today's conference call.

I would like to point out that we've posted a presentation on our website under the investor relations page to assist you in following along with the call.

With me today is Rich Montoni, Chief Executive Officer, David Walker, Chief Financial Officer, and Bruce Caswell, President and General Manager of the Health Services Segment.

Before we begin, I'd like to remind everyone that a number of statements being made today will be forward-looking in nature. Please remember that such statements are only predictions and actual events and results may differ materially as a result of risks we face, including those discussed in Exhibit 99.1 of our SEC filings. We encourage you to review the summary of these risks in our most recent 10-K filed with the SEC.

The company does not assume any obligation to revise or update these forward-looking statements to reflect subsequent events or circumstances.

Today's presentation may contain non-GAAP financial information. Management uses this information in its internal analysis of results and believes that this information may be informative to investors in gauging the quality of our financial performance, identifying trends in our results and providing meaningful period to period comparisons.

For a reconciliation of non-GAAP measures presented in this document, please see the company's most recent quarterly earnings press release.

And with that, I'll turn the call over to Dave.

Mr. David Walker: Thanks, Lisa, and good morning.

This morning, Maximus reported another quarter of strong growth, reflecting the contributions of work coming online from new products as well as ongoing expansion on existing contracts.

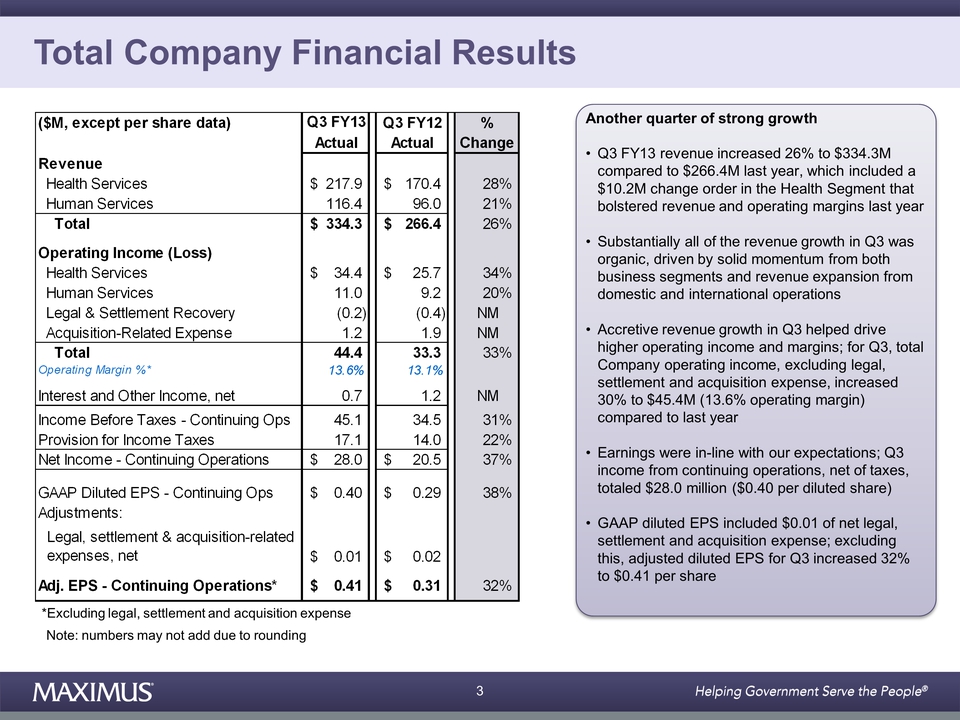

For the third quarter of fiscal 2013, total company revenue increased 26 percent to $334.3 million compared to $266.4 million reported for the third quarter of last year. As a reminder, the prior year period included a $10.2 million change order in the health segment that bolstered revenue and operating margins. Substantially all the revenue growth in the quarter was organic, driven by solid momentum from both our business segments as well as a nice mix of revenue expansion from both our domestic and international operations.

Accretive revenue growth in the third quarter helped drive higher operating income and margins. For the third quarter, total company operating income, excluding legal, settlement and acquisition expense, increased 30 percent to $45.4 million compared to the same period last year. This reflects an operating margin of 13.6 percent for our fiscal 2013 third quarter.

On the bottom line, earnings were in line with our expectations. For the third quarter, income from continuing operations net of taxes totaled $28 million, or 40 cents per diluted share. This included 1 cent of net legal settlement and acquisition expense.

Excluding this, adjusted diluted EPS for the third quarter increased 32 percent to 41 cents per share.

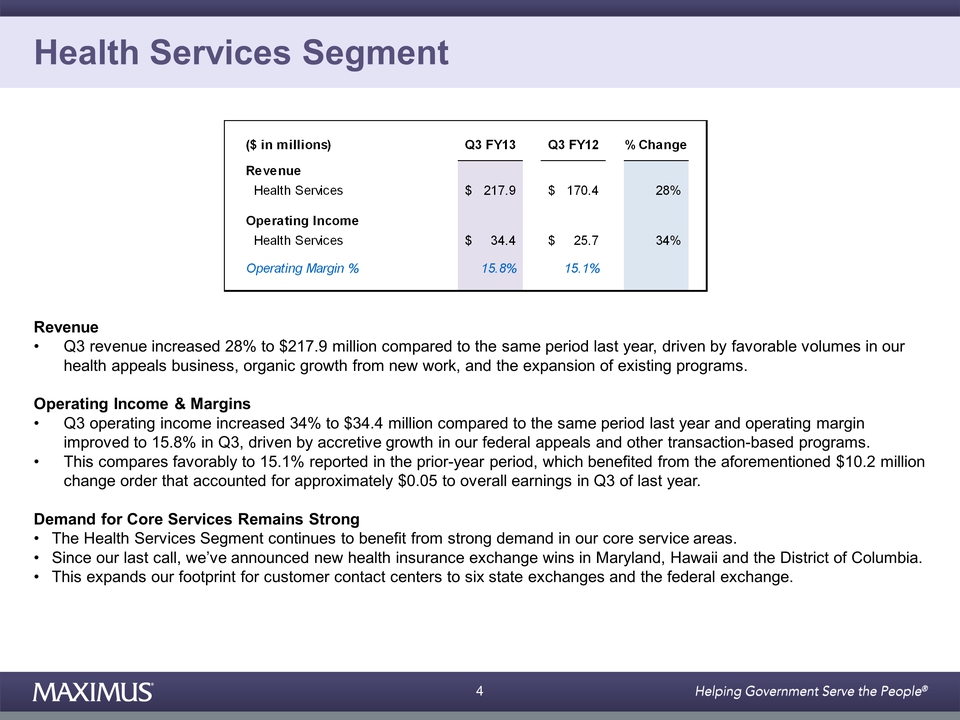

Let's jump into results by segment starting with health services. For the third quarter, health services revenue increased 28 percent to $217.9 million compared to $170.4 million for the same period last year. This top line increase was driven by favorable volumes in our health appeals business, organic growth for new work and the expansion of existing programs.

Operating income for the health services segment increased 34 percent to $34.4 million compared to $25.7 million reported for the same period last year.

Operating margin improved to 15.8 percent in the third quarter of fiscal '13, driven by accretive growth in our federal appeals and other transaction based programs. This compares favorably to 15.1 percent reported in the prior year period, which benefited from the aforementioned $10.2 million change order that accounted for approximately 5 cents of earnings per share to overall earnings in Q3 last year.

All in all, the health services segment continues to benefit from strong demand in our core service areas.

Since our last call, we've announced new health insurance exchange wins in Maryland, Hawaii and the District of Columbia. This expands our footprint for customer contact centers to six state exchanges and a federal exchange. Rich will provide further operational details on our progress with these important new programs.

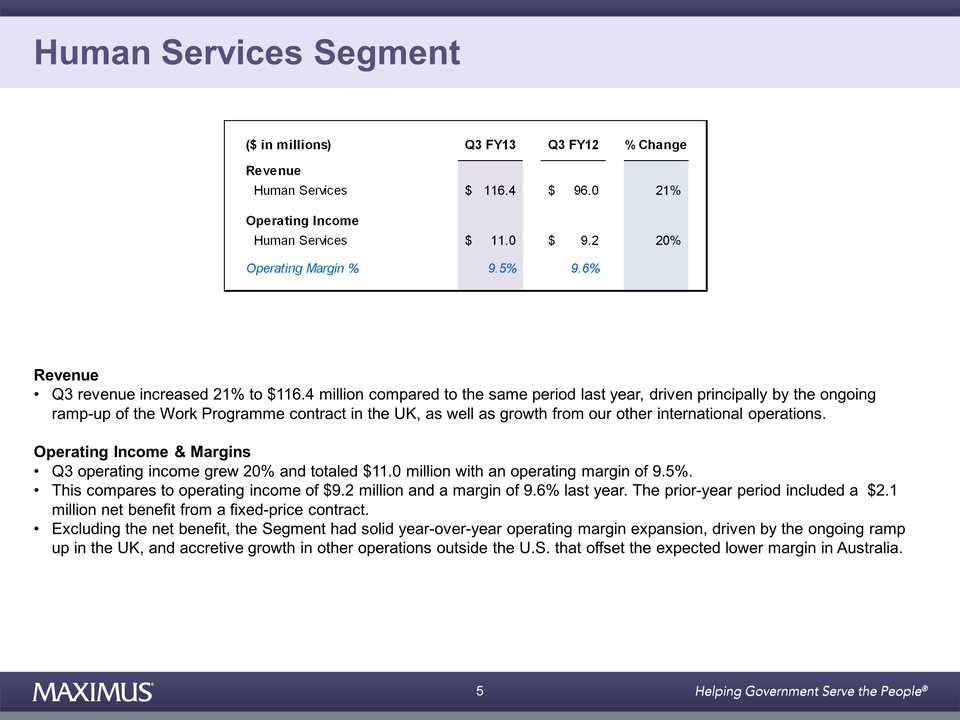

Let's now turn our attention to financial results for human services. For the third fiscal quarter, revenue for the human services segment increased 21 percent to $116.4 million compared to $96 million last year. For the third quarter, revenue increases for the human services segment were driven principally by the ongoing ramp up of the work program contract in the U.K. as well as growth from our other international operations.

Human services operating income for the fiscal third quarter grew 20 percent and totaled $11 million with an operating margin of 9.5 percent. This compares to operating income of $9.2 million and a margin of 9.6 percent last year.

As a reminder, the prior year period included a $2.1 million new benefit from a fixed price contract. Excluding this, this segment had solid year-over-year operating margin expansion, driven by the ongoing ramp up in the U.K. and accretive growth in other operations outside the US that offset the expected lower margin in Australia.

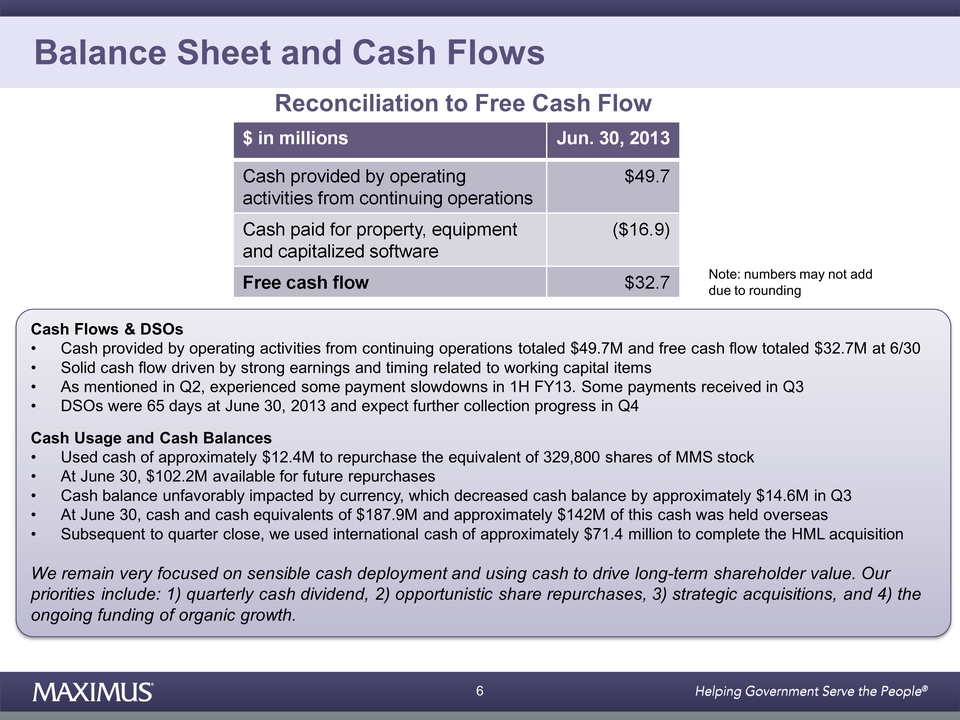

Moving onto cash flow and balance sheet items - cash provided by operating activities from continuing operations totaled $49.7 million for the third quarter, and we generated free cash flow of $32.7 million. This solid cash flow generation in the quarter was driven by strong earnings and timing related to working capital items and was consistent with our expectations.

As I mentioned on our last call, we had a couple of payment slowdowns in the first half of the year. As expected, we received some of the payments in the third quarter, and as a result, our DSOs improved sequentially to 65 days. We anticipate further collection progress in the fourth quarter, some of which we've already received.

During the quarter, we also used cash of approximately $12.4 million to repurchase the equivalent of 329,800 shares of Maximus common stock. And on June 30th, 2013, we had $102.2 million available for future repurchases under our board authorized share repurchase program.

Our cash balance was unfavorably impacted by currency exchange rates. Because the US dollar has been particularly strong, most notably in relationship to the Australian dollar, translation differences decreased our cash balance by approximately $14.6 million in the quarter.

Our strong cash flow more than offset this decline, and at June 30th, we had $187.9 million in cash and cash equivalents. Approximately $142 million of this cash was held overseas. And subsequent to quarter close, we used international cash of approximately $71.4 million to complete the acquisition of Health Management Limited, or HML.

We're very excited about this international acquisition because it broadens our existing operation in the UK as we extend our core competencies into this important market. We see real promise to serve more programs and capitalize on the opportunities we see intersecting between both our health and human service offerings. Rich will talk about this in greater detail in his prepared remarks.

We remain very focused on sensible cash deployment and using our cash to drive long term shareholder value. Our priorities include our quarterly cash dividend, opportunistic share repurchases, strategic acquisitions and the ongoing funding of organic growth.

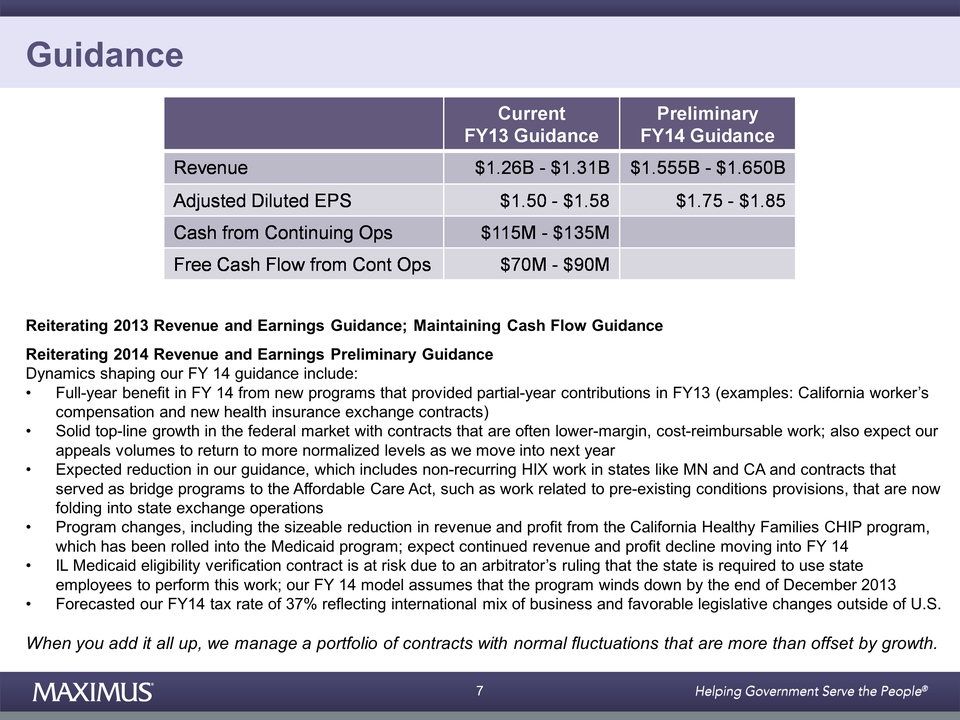

And lastly, Maximus is reiterating its fiscal 2013 revenue, earnings and cash flow guidance. The company continues to expect fiscal 2013 revenue to range between $1.26 billion and $1.31 billion and adjusted diluted earnings per share from continuing operations to range between $1.50 and $1.58.

The company continues to expect cash provided by operating activities from continuing operations to range between 115 million and $135 million.

Due to organic growth in the business and new programs ramping up, we now expect that our capital spending will exceed our prior CapEx guidance. Despite this increase, we still expect that our free cash flow from continuing operations will fall within our guidance range of 70 million and $90 million but more likely towards the lower end of that range.

Maximus is also reiterating its preliminary fiscal year 2014 revenue and earnings guidance, which includes the contributions from the acquisition of Health Management.

Let me provide some color on our fiscal year '14 preliminary guidance that we issued on July 1st. Our preliminary guidance is a tops down view based upon the facts and circumstances that we know today. We'll complete our formal bottoms up planning process later this month, and we'll provide final guidance on our November call.

So, let me outline some of the dynamics shaping our fiscal year '14 guidance. Let's start with the many positives.

As you know, we have a record number of programs that started this year and provided partial year contributions in fiscal year '13. We will now receive a full year benefit from all this new work in fiscal '14, and our forecast reflects these contributions based upon our current optics. These programs include our independent review services for the California Workers Compensation Program as well as the customer contact center operations for the six state based exchanges and the federal marketplace.

We also made significant headway in building up our US federal operations with several key wins in the books.

While we are seeing solid top line growth in the federal market, the contracts are often lower margin cost reimbursable work. We also expect our appeals volumes to return to more normalized levels as we move into next year.

We also factored some expected reductions into our guidance. This includes non recurring HCS [sp] work in Minnesota and California.

Additionally, contracts that served as bridge programs to the Affordable Care Act such as work related to preexisting conditions provisions are now folding into state exchange operations.

We've also talked about program changes including the reduction in revenue and profit from the California Healthy Families CHIP [sp] Program, which has been rolled into the Medicaid program. We expect continued revenue and profit decline from this program moving into fiscal year '14.

In addition, a recent development in Illinois has put our new Medicaid eligibility verification contract at risk. In June, an arbitrator ruled that, under the Union's collective bargaining agreement, the state is required to use state employees to perform this work. Right now, our model assumes that the program winds down by the end of December.

And finally, we are forecasting our fiscal year '14 tax rate to improve to 37 percent from our current year rate of approximately 38 percent. This reflects our international mix of business and favorable legislative changes outside the US.

So, when you add it all up, it's important to remember that we're managing a portfolio of contracts. And while we do experience some normal course fluctuations in the portfolio, the growth drivers more than make up for the reductions. And we're quite pleased with the top and bottom line growth targets that we've laid out for our fiscal 2014.

At this time, the company continues to expect that fiscal year 2014 revenue will increase 21 percent to 28 percent and range between 1.555 billion and $1.650 billion.

On the bottom line, we expect earnings growth between 14 and 20 percent and that diluted EPS will range between $1.75 and $1.85.

So, overall, fiscal 2014 is shaping up to be another great year of double digit top and bottom line growth for Maximus.

And with that, I'll hand it over to Rich.

Mr. Rich Montoni: Thanks, David, and good morning, everyone.

This quarter's financial results are right in line with our growth trajectory for the remainder of fiscal 2013 and set a solid platform for continued top and bottom line growth next fiscal year. We're pleased to be targeting double digit growth for fiscal 2014 as we continue to benefit from macro drivers and solid demand trends in our core markets.

Let's start off this morning with an update on our US health operations. Here, we have exceeded our initial goal for work related to the Affordable Care Act. With many new ACA related contract wins under our belt, Maximus has successfully established the leading position in the state based health insurance exchange market.

Maximus will be operating the customer contact centers for six of the 16 state based exchanges, including Connecticut, the District of Columbia, Hawaii, Maryland, New York and Vermont.

As we mentioned last quarter, we are also part of the team selected for the contact center operations contract for the federal marketplace.

We estimate that all of this new work adds up to more than $150 million new annual contract value. This exceeds the target goal that we laid out of winning 20 to 25 percent of the total addressable market of approximately $500 million in new annual contract value.

So, we're pleased to have secured our fair share and a little bit more of health insurance exchange work.

Operations for these new contracts are ramping up nicely. The Maryland HCS customer contact center went live last week, and our professionals are already hard at work answering general inquiries about the Affordable Care Act and health insurance exchanges. They're also helping consumers prepare for the open enrolment period that commences on October 1st.

We are operating two customer contact centers for the federal marketplace. Our Brownsville, Texas location also launched operations last week, and our customer service representatives are already taking calls.

The build out of our second site in Boise, Idaho is progressing as planned, and the team will be ready for open enrollment in October.

The build outs of our remaining exchange contracts are on track. Hiring is progressing as expected. And our training teams are gearing up to prepare our customer service representatives for incoming calls.

We are pleased with the overall progress, and Maximus will be operations ready to support our government clients for the October 1st open enrollment.

Additionally, we will continue to assist our current state clients who are defaulting to the federal marketplace as they strive to meet ACA requirements, including the no long door [sp] provisions.

So, with our new exchange operations on track, we remain keenly focused on the next wave of ACA related opportunities. Right now, we see a landscape developing where, over the next several years, many states will likely consider additional initiatives including the expansion of Medicaid and other health provisions under ACA.

So, as we've stated all along, health care reform will be a long term, multi year growth driver for Maximus, particularly as the different health insurance marketplaces evolve over time.

Moving onto our international operations, the acquisition of Health Management in July was an important next step for introducing our core health offerings to the United Kingdom. Health Management is the largest independent occupational health provider in the United Kingdom. Their services include health assessments, sickness absence referrals and management services, wellness programs, primary care and well being services and employee assistance programs.

Health Management brings a team of recognized and highly qualified occupational health consultants to Maximus. Health Management is a great fit for Maximus because both companies share many of the same fundamental values. We are both keenly focused on providing our clients with innovative solutions to address their health, social and productivity challenges.

By coupling our core independent review competencies developed in the US with an established proven partner in the UK, we've created an exceptionally strong delivery team that is well positioned for future opportunities. The acquisition of Health Management demonstrates our commitment to serving more clients in this important market and working with the UK government to achieve its program goals.

As we mentioned last quarter, we see emerging opportunities that may lead to RFP activity during fiscal 2014, so we are very excited to further enhance our offerings in existing markets to create new long term growth platforms.

Our expansion in the United Kingdom builds upon the positive reputation and solid performance by our UK Welfare to Work team remaining one of the top performing vendors under the work program, the position that was most recently highlighted in the vendor statistics issued in late June.

Let me give you a general update on what's happening with the work program. Since we started the contract in July 2011, referrals into the work program have been lumpy. However, as we've gained additional experience on the program, we've achieved confirming data points that provide us with better trend data, improved our overall visibility and allow us to refine our operational and financial models.

As you may recall from our disclosures in fiscal 2012, we initially saw higher case load volumes. However, since the start of the program year two in April 2012, we've experienced overall referrals that are lower than the forecast initially laid out. We initially thought volumes would return to more normalized levels based upon our prior experience. But, volumes remained lower than expected, which led to lower revenue levels.

Despite the lower revenue, we have successfully managed to remain in line with our net income expectations. The team has done an excellent job of managing resources and labor.

This is all factored into our current 2013 guidance as well as our preliminary guidance for fiscal 2014.

There's also been interest in how future reallocations might work. The Department for Working Pensions has two models for reallocations. First, they can do intra region reallocations, which is a shift of case load within the regions that we already operate.

DWP has stated that the intra region reallocations would only shift up to 5 percent of case loads to other qualified vendors within that region. This shift is immaterial to Maximus and would account for less than $500,000 in new annual revenue in the regions we currently serve.

The second type of reallocation is an inter region reallocation. In this case, a qualified high performing vendor can pick up an entirely new region if they are in the framework for that particular region. At this time, it's unclear what the timing on this inter region reallocation may be, but we don't believe there will be any material reallocation of work in the near term.

And I want to further reinforce what we've been saying from the beginning of this program - our interest in picking up any new regions is contingent upon the overall terms and conditions of the contract.

So, while we think reallocation opportunities exist down the road and are an important part of our land and expand strategy, we're far more excited about the many new promising opportunities that we see starting to materialize for new programs and new work in the UK. Our current operations combined with our acquisition of Health Management create the springboard for many of those longer term Greenfield opportunities.

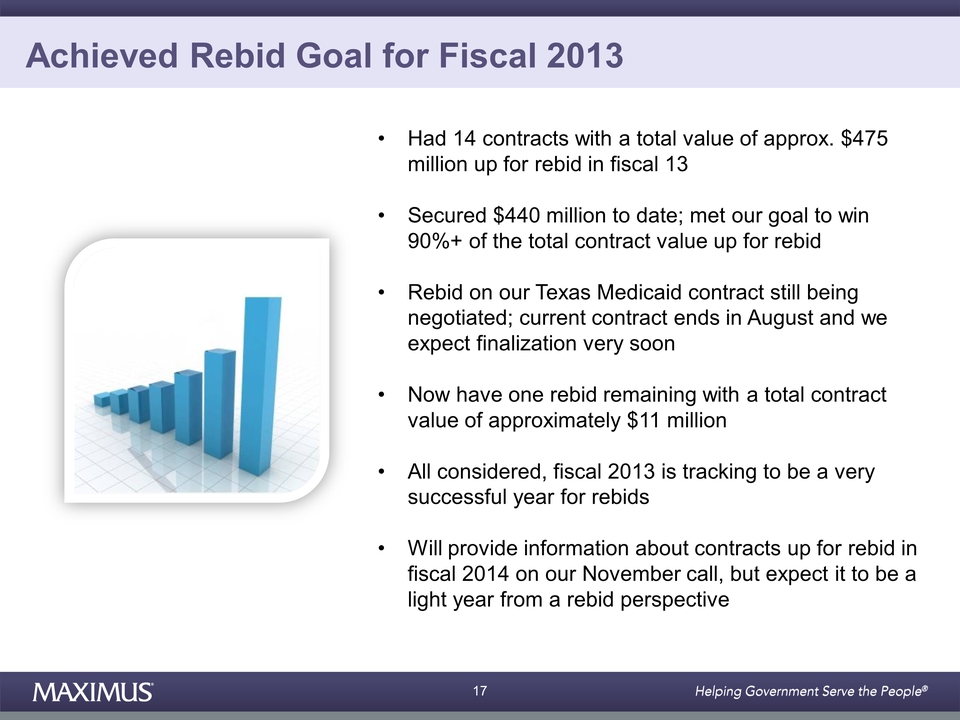

Turning now to rebids - we had 14 contracts with a total value of approximately 475 million up for rebid in fiscal 2013. We’ve secured 440 million to date and have met our goal to win 90 percent plus of the total contract value up for rebid. The rebid on our Texas Medicaid contract is still being negotiated. However, our current contract ends in August, so we expect finalization of the contract very soon.

So, at this point in time, we now have one rebid remaining with a total contract value of approximately $11 million. So, all considered, fiscal 2013 is tracking to be a very successful year for rebids.

We'll provide information about the contracts that are up for rebid in fiscal 2014 on our November call, but we expect it to be a light year from a rebid perspective.

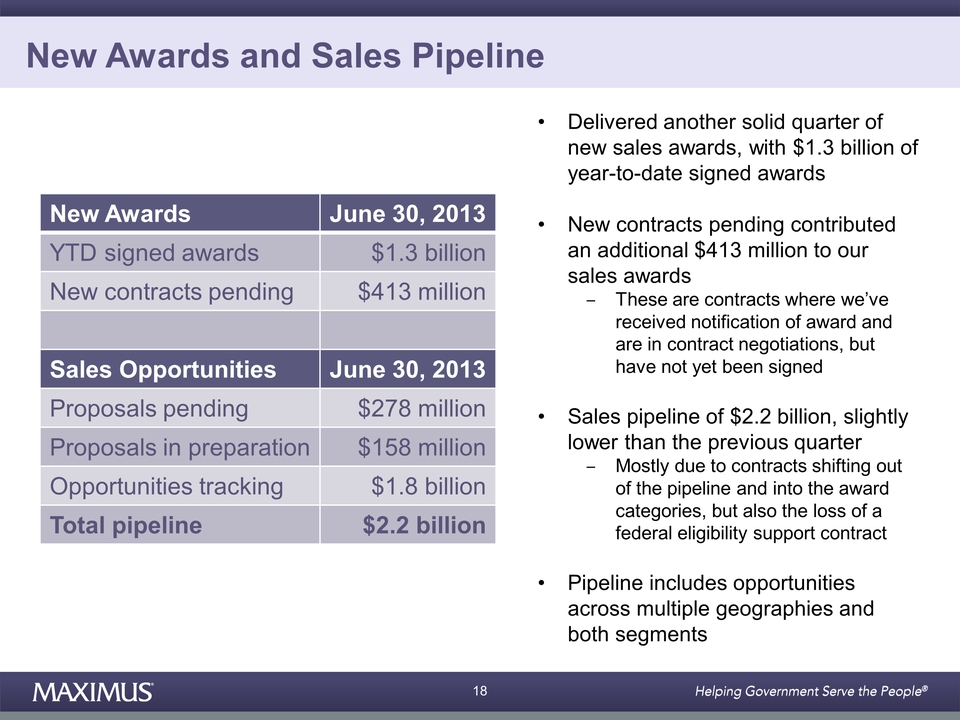

Moving onto new sales award in the pipeline - we delivered another solid quarter of new sales awards with 1.3 billion of year-to-date signed awards at June 30. New contracts pending contributed an additional 413 million to our sales awards. These are contracts where we have received notification of award and are in contract negotiations that have not yet been signed.

Sales pipeline at June 30th, 2013 was $2.2 billion, which is slightly lower than the previous quarter, mostly due to contracts shifting out of the pipeline and into the award categories, but also due to the loss of a federal eligibility support contract. The pipeline includes opportunities across multiple geographies in both segments and consists of $278 million in proposals pending, $158 million in proposals in preparation, and $1.8 billion in opportunities tracking.

In closing, we continue to make steady meaningful progress towards our three pronged long term growth strategy, which includes securing our fair share of healthcare reform work in the US, growing our federal book of business and expanding our international operations.

We are proud of the team's achievement in securing our fair share of the first wave of health insurance exchange contracts, and we remain optimistic about other long term opportunities in the other areas of healthcare reform.

The acquisition of Health Management has provided Maximus with a strengthened position for future opportunities in the UK health market. It also supports our international growth objectives as we expand our service offerings and our geographic footprint.

It's important to keep in perspective that our long term growth is not dependent upon a single business area or geography but rather upon macro trends and extended growth drivers. We see many new emerging opportunities for our core capabilities in all of our geographies, and with our fiscal 2014 preliminary guidance in place, we remain committed to generating long term shareholder value as we continue to grow the business.

And with that, let's open it up for questions. Operator?

Operator: Thank you.

We will now be conducting a question and answer session.

Please limit your questions to two. If you wish to ask additional questions, you may reenter the queue.

If you would like to ask a question, please press star, one on your telephone keypad. A confirmation tone will indicate your line is in the question queue.

You may press star, two if you would like to remove your question from the queue.

For participants using speaker equipment, it may be necessary to pick up your handset before pressing the star keys.

One moment please while we poll for questions.

Thank you.

Our first question comes from the line of Charles Strauzer of CJS Securities. Please proceed with your question.

Mr. Charles Strauzer: Hi, good morning.

Mr. Rich Montoni: Good morning, Charles.

Mr. Charles Strauzer: Rich, if you could expand a little bit more on the HML acquisition--I know it's one that kind of slipped through the cracks a little bit, given the, uh--some of the noise about a large federal contract. But, um, talk to me about, A, the rationale behind the, uh, the acquisition a little bit more, and also if you can maybe frame the opportunities, the market opportunity, I should say, um, that's, you know, kind of behind, you know, the rationale there.

Mr. Rich Montoni: Uh, Charles, be glad to do that. As a starting point, um, what I would say is back up a little bit and recall our discussion in terms of what our international expansion strategy is.

And we actually have a four phase, uh, expansion, uh, strategy. And the fourth phase is, once we've established a single significant program in a new geography, uh, their initial task is to establish themselves as a leading provider, a credible provider, good brand in the community, known by the government officials and then use that to springboard and offer additional services - uh, i.e., phase four - to that government, again, piggybacking on the brand, the reputation, uh, we established during phase three.

And in the case of the UK, uh, phase three was really--the charge was led by our human services, uh, team who established and won--you may remember two, three years ago, uh, that initial win with the work program, and the team has done from day one and continues to do a great job to serve that client and built a great brand. Uh, that team worked with our health services folks to identify opportunities, health related opportunities in the UK.

And in this particular case, it became clear the best way to take advantage of what we think are growing opportunities in the UK was to make an acquisition. And, uh, working with our M&A team, our health and human services folks, um, all worked to sort through the likely candidates, what was available and, uh, were very, very fortunate to be introduced to HML and come to terms to acquire HML.

And it really is a, just a first class organization, uh, just from, uh, an operational perspective and a diligence perspective, and it's a company that has great, great people who are very much focused on the same values as Maximus, and that's quality service to its clients. It has a good reputation, uh, within the government already.

Uh, so it's a great I'd say adjacency for us and really puts us, when combined with HML, into a great position to win some opportunities in the UK, which we think will occur over the next several years.

I won't get into particular opportunities, uh, but I do say that that's a government that does procure on a central basis, um, programs for which, uh, now HML with Maximus is very, very well positioned to serve that government. So, we're excited about it.

Mr. Charles Strauzer: And, Rich, I know you can't really, you know, talk about specific opportunities, but is there a general sense of maybe the market opportunity that you could maybe share with us?

Mr. Rich Montoni: Uh, you know, in terms of market opportunity, I think there's just a cadre [sp] of services that fall within, um, welfare programs and health programs for the UK government. It's interesting in the UK. I mean, effectively, these programs, um, are run under the same department, uh, so our existing client.

So, whether it's, uh, similar to what we do here in the US in terms of processing appeals, um, assessments and, uh, really just running the back room of these programs, uh, would be the general opportunity for us.

Mr. Charles Strauzer: Great.

And then, my follow up is just, uh, sitting at the national view, when you look at the Saudi Arabia pilot program there, you know, can you give us an update on the next phase there?

Mr. Rich Montoni: Oh, boy, that's a real dynamic country in terms of the changes that are occurring from a social level, uh, in many, many, many dimensions. And, uh, I think the team's done a good job on this pilot program. We're in active negotiations to extend the pilot and renew the pilot. So, we're very, um, confident that, um, those discussions are advancing as planned.

And I do think, longer term, there will be additional opportunities for Maximus above and beyond that single program.

Mr. Charles Strauzer: Great. Thank you very much, Rich.

Mr. Rich Montoni: You bet, Charles. Thank you.

Ms. Lisa Miles: Thanks, Charlie.

Next question please.

Operator: Next question is from the line of Carl McDonald with Citigroup. Please go ahead with your question.

Mr. Carl McDonald: Great, thanks.

Um, be interested if you could talk a little bit about the composition of the pipeline. As you mentioned, you've had a lot of contracts leave the pipeline and be awarded, so just be interested if that mix of business within the pipeline has changed to any significant degree in terms of the types of contracts that are in it.

Mr. Rich Montoni: Um, good morning, Carl. This is Rich.

Um, you know, I don't really see a meaningful shift. It's not as if it's shifted to bias towards one segment or one geography. I do think that we have strong opportunities here in the US.

The US is biased perhaps towards health. Uh, but otherwise, uh, I see strong growth opportunities geographically, uh, growth plans for Canada, UK, US, yes, with a bias towards health and Australia - so, across all of our geographies.

And, um, I'd say in the other countries, you'll find perhaps a bias towards human services is one--in one. But, again, let's be clear - a long term growth strategy, and I'd like to say it's the land and expand examples we've set in Canada and Australia and, um, we're now in process in the UK--uh, we seek to have a meaningful book of business in both segments.

Mr. Carl McDonald: And then, uh, a separate question on the forecasting - uh, when you look at your, uh, top down versus your bottoms up analysis, uh, where do the biggest variances, uh, tend to occur between, uh, between those two different perspectives?

Mr. Rich Montoni: Uh, Dave Walker is with us today, and I'm gonna deflect this one to Dave and ask him for his initial thoughts on that.

Mr. David Walker: Well, uh, top down versus bottom's up - I mean, if the bottom's up, and remember, it happens in the next week, and then we'll roll forward to November, it'll start by, you know, what's in the pipeline. That has yet to be decided, and there's a few things that can move that, and that helps us.

You also have to appreciate, when we do the bottoms up, we have at least a few more months of operating history, and that's helpful for us to gauge future operating income for things that are in startup phase.

So, you know, I think we're pretty good at hitting the mark, you know, where we think it is. Uh, but sometimes, they start a little slower, we assess where that is and that helps us do that. So, those are the sort of items that cause us to reconcile the two.

Um, and then if we get differences between the segments, we do have a lot of discretion in terms of what we spend on business development, you know, and how we support organizations. So, we have the ability to always adjust our SG&A, um, and our selling costs to adapt to what we think to be an appropriate business space in the markets we want to address. So, that's where we'll reconcile all that and square it up.

Mr. Rich Montoni: Carl, I would add this to David's comment - uh, the tops down is, I think, a bit more firm than many tops down. In some tops down, you'll just see a macro what do we think the market's growing at, and that becomes our tops down placeholder.

Mr. Carl McDonald: You bet.

Mr. Rich Montoni: Uh, this is a situation where, when we do a tops down, Dave Walker and his team, they will identify down to, uh, more material projects what we see as new work next year and work that might be phasing out or big projects that are going into maintenance mode. Uh, so we do start to get a bead on that.

Uh, the difference between the tops down in our final number is we do go into, um, uh, a division by division review of the division leadership's forecast, where we want to make investments, um, where we want to pursue new business and really provide a second guess, if you will, on a division by division basis, major program by program basis.

So, the tops down differs from, uh, the bottoms up in that the bottoms up is just more of a real scrub of the data as we know it. And obviously, we're closer to the beginning of the year than when we perform our tops down.

Mr. Carl McDonald: Uh-huh.

Mr. Rich Montoni: Is that helpful, Carl?

Mr. Carl McDonald: Yes, that's great. Thank you.

Mr. Rich Montoni: Yep.

Ms. Lisa Miles: Next question please.

Operator: Next question is from the line of Frank Sparacino of First Analysis. Please proceed with your question.

Mr. Frank Sparacino: Hi, guys. Uh, I wanted you to go back to the UK work program and just get a sense of what factors are impacting the business there and how much of that is related to the economy, but also just get a better sense--uh, I think in the original projections for that contract, you know, the operating margin was in the 16 percent range. And, uh, just curious where you think that'll be going forward if, in fact, uh, the lower, uh, volume in revenue trends persists.

Mr. Rich Montoni: Uh, Frank, this is Rich. Um, I think this - I think it's helpful to, um, to separate the top line or revenue dynamics in a work program from the bottom line. And it makes the point about the nature of the model.

Uh, from a top line perspective, the biggest variable based on the original plan, and the original plan was based upon estimates provided to all the bidders by the UK government, the referral levels are down in comparison to their estimate.

So, we started the program where actually referrals were greater than the estimates. You may recall some quarters where we shared that with you.

Um, but year-to-date in the most recent year, the referrals are down. And that's the beginning of the pipeline. So, you need to feather [sp] that through and when you do model that through, um, and there is a delay because, you know, the larger pay point is not when we find a referral a job but when they've been in that job.

So, um, as it relates to the bottom line, uh, the good news is the program is such that, um, most of our cost, which is labor, is variable. And we monitor that very, very closely. I think that's the difference between a first class operator and those who are, uh, an ability to have a right amount of, uh, customer service representatives, uh, focused on the cases that we have.

And the team's done a great job, such that, from a bottom line perspective, it is exactly where we expected it to be from an operating, uh, income percentage. Uh, it's the upper end of the range. So, I have no complaints with the program in that context.

And, you know, the government had an initial best estimates as it relates to referrals. We can speculate why referrals are lower. Um, it's economic in nature, and it's also just the referrals that the government in reality had available.

And, you know, I do know that there's an intent and discussions between the industry, including Maximus and the client, to work on those referrals. Fingers crossed - they may increase. But, it's difficult to forecast.

Does that help, Frank? Okay.

Mr. Frank Sparacino: It does. Thank you.

Mr. Rich Montoni: Okay.

Next question please.

Operator: Your next question is from the line of Brian Kinstlinger of Sidoti and Company. Please proceed with your question.

Mr. Brian Kinstlinger: Hi, good morning.

Mr. Rich Montoni: Good morning, Brian.

Mr. Brian Kinstlinger: So, the first question I've got, if I exclude one time items and I assume 2Q is the bottom for the operating margin in human services, given we saw full effect of Australia's changes, I would have expected a little bit more of a bounce in 3Q in the volumes than based on what you just said, uh, that you're hitting your targets on, uh, margin, uh, in that program.

So, I guess I'm curious why we didn't see a little bit more of a bounce sequentially, and should we expect margins to improve with volume increases over the next few quarters, if they do increase?

Mr. Rich Montoni: Okay.

I'm gonna ask Dave Walker--you've got a two part question, I think, uh, one, why were margins not greater in human services segment this quarter and then, uh, what do we expect on a go forward basis, particular Q4.

Mr. David Walker: Sure. Hey, uh, thanks, Brian. Uh, great question.

Uh, well, so actually, sequentially, you know, the profit grew 4.3 percent, you know, and the revenue 3.6, so it did increase. And the UK, which in fact is at an operating income is pretty consistent with our operation, is jut a piece of the pie. And the pie isn't staying still. You know, remember, we threw a lot of domestic growth with the PSI acquisition in there, and the other programs are growing nicely.

So, I would say the UK is at the higher end of the portfolio range. Uh, and there is volatility, you know, within programs quarter-over-quarter.

Uh, and in fact, just as a reminder, Q4, we--is generally heavily driven by seasonality in both health and human services. And I think human services, you'll see the biggest sequential growth in Q4. You know, and again, that's driven by--we see seasonality in MAX Network, we see it in tax credit, um, and timing of change orders.

So, um, so we will see it go up. But, again, I think the UK is just a piece of the pie. And the UK as the bigger piece of that pie has been relatively flat. Okay.

Ms. Lisa Miles: Uh, just for your, um, perspective, Brian, MAX Network is Australia.

Mr. David Walker: Oh, yes, I'm sorry.

Um, and when you look into next year, you know, I think all of the businesses are gonna grow nicely, and we expect sequential growth. And I think UK will have its share. And in order for it to contribute more margin, it would need to grow at a faster rate, and we're not seeing that at the time. We're seeing growth across the board. So, I would expect our margins to maintain within our guidance that we currently have.

And if I just looked at them relatively speaking, generally speaking, health where we think we'd have the greatest differentiation will be at the higher end of our margin range and human will tend to be at the lower end of our margin range. But, they've been about equal over the last year or so.

Mr. Brian Kinstlinger: That's helpful.

Um, my follow up is, hypothetically, if you were not to win the federal appeals contract, what would happen to your '14, uh, revenue and EPS guidance? And I guess, would it suggest--I know you factor them but, uh, would it suggest you'd probably be more towards the low end and likely a shortfall?

And it seemed that your proposals pending wasn't that high given this outstanding RFP. So, I'm curious about that.

Mr. David Walker: Well, I guess I'll answer it two ways for you. Um, one, we would still be within the range. So, that's why we give a range, and that's why it's so broad, you know, this early in the year.

Um, so, um--and I would say the second part of it is not to forget that's a cost reimbursable contract. So, I have two ranges I've given you - revenue and operating income.

And I'm more confident of my ability to work my operating income than I am the top line of low margin, you know, business that's reimbursable.

So, as you know, we perform best when it's operation based, um, and when it's outcome based. And so, we're glad to take the reimbursable revenue, but it is not our favorite.

Mr. Rich Montoni: One thing I'd like to add to this, um, and that is what I refer to as the one year phenomenon. When we present, uh, pipeline information, um, our protocol is just to include the base year. And of late, we've seen a trend with the federal government--the base contract, rather, base contract value--uh, we've seen a trend with the federal government whereby what they've been doing is going out with a one year base contract with multiple, three, four, five, eight plus option years. For all practical purposes, that will likely end up being a multiple year contract arrangement. Um, but the federal government is going with a one year base.

So, um, it's difficult to discern that. When you look at the pipeline information, uh, it would be included as a one year contract value--.

Mr. Brian Kinstlinger: --Okay--.

Mr. Rich Montoni: --So, keep that in mind.

Mr. Brian Kinstlinger: Yeah, that's helpful, thanks.

Mr. Rich Montoni: Okay.

Ms. Lisa Miles: Uh, next question please.

Operator: Next question is coming from the line of Brian Hoffman of Avondale Partners. Please proceed with your question.

Mr. Brian Hoffman: Good morning. Thank you for taking the questions.

Uh, I've got--uh, my first question is on the healthcare claims appeals business. You mentioned that, uh, this should return to more normalized levels. Can you talk a bit about what's going on here and driving this change and when you, uh, expect, uh, normalized levels to start to appear?

Mr. Rich Montoni: Oh, glad to do that, Brian. And I'm gonna hand this over in a minute to Bruce Caswell, who I believe you know runs our health segment, and Bruce is, uh, closely tied to what's going on with, uh, our federal business and appeals. And we're real happy that it's been a great contributor to all of this year.

Uh, but to be clear, when we say more normalized levels, the volumes in that business over the last year have spiked significantly. And every quarter, uh, we've seen significant increases.

We think it's going to level off in terms of increasing but level off at the higher level. Uh, we--I don't expect that it's going to go back to what it was, uh, in years past. So, it's more leveling off than back to normalized levels.

So, with that perspective, I'm gonna hand this over to Bruce and any comments you'd like to share about what's going on in the appeals world, if you will.

Mr. Bruce Caswell: Sure. Brian, good morning. Um, I think, first of all, as you're, uh, probably quite aware, it's difficult to predict future volumes. There are a lot of factors that can affect, uh, the volumes in the appeals world - um, certainly, the ongoing debate around how Part B of A claims are gonna be handled based on the interim final rule that was, uh, issued in March, you know, has the hospital community lobbying hard for less restrictive rebilling rights there.

Um, if anything, you can maybe attribute a little bit of the leveling off--and again, leveling at a much--at a high level--uh, to some of those dynamics with maybe fewer, uh, B of A appeals and more claims being just billed as part B.

But, counter balancing that, as you're probably aware is that the, uh--about a year ago, CMS allowed direct contractors to expand their work to prepayment audits. Uh, and that prepayment audit program really only covered 11 states.

And so, there's some speculation, uh, and I think it's based on strong, um, evidence that that's been a successful program, that that, uh, prepayment audit program could be expanded, um, to a much larger, um, set of states. So, that would provide obviously a bit of a tailwind.

And then, finally, um, there's the dynamic just around the whole rack reprocurement, uh, process where, as you're aware, the reprocurements were intended to, uh, transition contracts in the February to April timeframe of next year, uh, but there's even late breaking news this morning that, um, some of the existing rack contracts are going to be getting extensions in terms of their ability to, uh, continue to submit claims and support the appeals process, suggesting that, um, any effect you might see, uh, or would expect in early 2014 would be pushed out.

So, uh, I think just to summarize, uh, Rich put it well when he said, while we've seen a leveling off, it's a leveling at a much higher level than historical volumes, and we've used that as the basis for our forward projections because it's really the best information we currently have.

Mr. Rich Montoni: Well, and to be clear, leveling off at a high level with it ramping up to the year mathematically, that means it's a growth driver in real dollars--.

Mr. Bruce Caswell: --That's right--.

Mr. Rich Montoni: --Uh, next year over this year.

Mr. Bruce Caswell: Yeah.

Mr. Brian Hoffman: Right.

Mr. Rich Montoni: Next question please.

Operator: Our next question is from the line of Brian Gisweli [sp] with Raymond James. Please proceed with your question.

Mr. Brian Gisweli: Yeah, good morning, guys.

Mr. Rich Montoni: Good morning.

Mr. Brian Gisweli: Um, Rich, wanted to dive into the pipeline one more time. Um, it strikes me that the international composition might be a little bit higher than what it was a year ago, uh, through growth there, but also the profitability mix of this might be a little bit higher as maybe, uh, more performance based contracts within the pipeline, uh, relative to what we saw on the federal side of things this year?

Mr. Rich Montoni: Oh, boy, Brian. I think that is a data point that's true. Um, uh, we do see increasing opportunities that are performance based.

Um, that being said, uh, you know, we've got a three tier, uh, growth strategy here - uh, health focusing, uh, in years past on US, now international, uh, federal, um, and then international, per se.

Um, in years past, there has been a tendency towards, uh, performance based contracts, hence higher margin. But, I will say we still have very significant growth aspirations for our federal business, some of which I think will be performance based, hence higher margins, some of which could be at the other end of the continuum, way at the other end of the continuum, really cost reimburse--uh, reimbursables, which would carry single digit margin.

So, uh, it's really difficult at this point in time to handicap what's in that pipeline from a profitability mix perspective.

Ms. Lisa Miles: I guess, Brian, I would add from a comparison to last year, as you recall, um, the pipeline was quite large at this quarter, uh, last year, um, much of it due to some of the opportunities we saw related to the Affordable Care Act. And so, if I pivot off that and look at this year, it's probably fair to say that, perhaps in this year's pipeline, we do see a greater number of international opportunities when we look at relative to last year.

Mr. Brian Gisweli: Great, that's very helpful.

Uh, maybe just, uh, a margin question, um, in the human services side of things - um, can you talk maybe to, uh, how Australia kind of progresses as a, what has been a headwind this year and maybe the timing of when it converts to begin to be a tailwind for the business, uh, after you kind of digest some of these investments that you've made?

Mr. David Walker: Well, I mean, I actually think, uh, MAX Network, uh, sequentially year-over-year was down, but it has certainly leveled off. So, we're actually seeing it if you look sequentially.

Um, it's kind of at the level that we think it will be, um, you know, as the government adjusts to those programs there. And we still think it's a program, um, where it will continue to drive the top line, um, through additional allocations of work, you know, and adjacencies, uh, that we've been successful in.

So--.

Mr. Rich Montoni: --I would add to that--I agree with Dave Walker's comments, and I would add to it. My view is that I think MAX Network, uh, really has stabilized, is in very much the growth mode.

So, you know, they've done a great job to deal with the programmatic changes that came about about a year ago. Um, I think we're done with the year-over-year impacts of that. I think they're growing top line and bottom line, and it's a solid performer. We've got a great management team down there. It has a great partnership with our client. Uh, they've had some nice wins and have a nice pipeline. So, I view it as a very solid, um, uh, growth business.

Mr. Brian Gisweli: Uh-huh. Okay, thanks.

Mr. Rich Montoni: Next question.

Operator: Our next question is a follow up from the line of Frank Sparacino of First Analysis. Please proceed with your question.

Mr. Frank Sparacino: Hi, guys, I just wanted to come back, uh, maybe Rich or Bruce, on, uh, state based exchanges and just curious, um--obviously, there's been a lot of criticism or skepticism on the federal side of things, but just curious where you think the six states are that you're working with, particularly New York, which is, uh, far and away the largest?

Mr. Rich Montoni: Um, thanks for the question, Frank.

And, uh, Bruce, what are your views on that?

Mr. Bruce Caswell: Well, I appreciate the question, Frank, and, uh, actually spent the day on Monday in Albany with the team that's standing up that operation. And I would say, across the board for the six states we're working with, uh, we are very much ready to go live, will be ready to go live, um, in October for open enrollment.

And then, as Rich mentioned in his script, we've already, in fact, gone live in two locations. Brownsville, Texas is part of the federal, uh, operation, and then in Maryland with a, uh, information line for general questions.

So, as we're looking at the states as they, you know, plan the last few months here to October 1st, um, invariably, as you--I'm sure you're reading, they're making tough choices and prioritizing, uh, on day one system functionality what's absolutely essential for the operations.

But, we have found across the board that our clients remain singularly focused on a positive consumer experience on day one. So, any kind of reprioritization of functionality generally leads to more work being done in the back office, uh, to ensure that the consumer experience is first class. And if anything, that could lead to more labor on our part handling additional, uh, manual tasks that then become automated through subsequent system fixes. So, we're feeling quite confident on--about day one operations across the board.

Mr. Rich Montoni: Next question please.

Operator: Thank you.

As a reminder, you may press star, one to ask a question, and we ask you please limit yourself to two questions.

The next question is a follow up from Brian Kinstlinger with Sidoti and Company.

Mr. Brian Kinstlinger: Good morning, again.

Um, the first question I've got is do you expect the Federal Exchange to be ready for open enrollments in October? And if not, do you think it'll be ready for enrollments January 1st?

Mr. Bruce Caswell: Like me to take that?

Um, Brian, it's Bruce. Thanks a lot for the question.

And, uh, again, you know our involvement in the Federal Exchange is really through our work, um, as a subcontractor [unintelligible] GDIT in the call center areas. And so, our optics, obviously, to, um, the readiness of several of the key platform areas like the Federal Exchange, uh, Platform System or FEP System, or the data services hub is limited to really probably about the same information you can pick up in the media.

Um, at the same time, a lot has been said about, uh, the progression of those efforts. Uh, there are states that have, uh, gone through now successful testing against the data services hub. There are standards being published for the things they call the account transfer objects, which is a critical element of how data will move between, uh, federally facilitated exchange operations and the state governments that retain, as you may know, an obligation to, uh, handle those Medicaid cases that come down from the federal level and provide the system of record.

So, there's, uh, you know, uh, what we would refer to as a complex orchestration that has to be completed between the federal level and the state level. And as, uh, Rich mentioned in his remarks, um, we're working hard to help our state clients that retain obligations related to the no loan door [sp] provisions of the act to ensure that their systems and operations are gonna be ready to handle those cases as they come down.

So, overall, um, I would just say that, you know, our efforts, um, bringing up in a timely manner the Brownsville operation last week, the ongoing, uh, fit up and, uh, readiness of the Boise operation suggests that, certainly from a call center perspective, again, we'll be ready on day one.

Mr. Rich Montoni: And, Brian, I would emphasize that, from Maximus' perspective, uh, we are doing everything, um, we can, and we will carry our fair share of responsibility on the Federal Exchange. But, there are very, very many moving parts, uh, many not, uh, the responsibility of Maximus.

So, it's difficult to handicap your questions in their entirety from our perspective. It's a great question, though. Thank you.

Mr. Brian Kinstlinger: The last follow up is two housekeeping items. The first is of the--of the HCS work you've won, how much is federal? And then, where is the increased CapEx going? It's one of your lower free cash flow years in a long time, so maybe highlight where that money is going.

Mr. Rich Montoni: It's a difficult one to answer in terms of the HCS components, Brian, because we're just not at liberty to expose the component parts. The clients are quite, uh, finicky about that. So, we're gonna have to decline, uh, responding to that one.

On the CapEx, uh, Dave Walker, we do have some dynamics on the CapEx level. What would be your commentary?

Mr. David Walker: Oh, it's very much startup driven. Um, so if you look at it, it is cap software that we have to put in place, and a good portion tends to be funded, but we have to defer that revenue, um, to in fact put these systems, these call center systems, phone switches, etc., into place.

So, it's a little bit you see it in the furniture and fixtures and you see it in the, uh, equipment. Uh, even the internal back office, our employee headcount has grown so fast, uh, that we actually had to book another license just to have software for our time carts.

Um, so it's all anticipated, and it's all tied to startup. And you can triangulate the revenue growth with how this stuff, uh, tracks. So, that's what it's tied to.

Mr. Rich Montoni: Good.

Now, we--thank you, Brian.

Uh, next question, please.

Operator: Next question is a follow up from the line of Brian Hoffman of Avondale. Please go ahead with your question.

Mr. Rich Montoni: Hey, Brian.

Mr. Brian Hoffman: Hey. Thanks for taking another question.

Can you tell us how much revenue growth in the quarter came from PSI and what sort of, uh, growth you're anticipating for PSI over the next year?

Mr. David Walker: Um, yeah, sure. Uh, just a sec.

I mean, virtually, if you look at it year-over-year, it--it's, uh, it's all organic growth, uh, materially. And, um, you know, and really, essentially, that means PSI decline year-over-year. And we expected that. When we purchased PSI, we did expect some decline due to client concentration.

So, uh, both entities would maintain all the combined work in certain program areas, and we've seen that to be true. Um, so, essentially, all the growth you're seeing materially is organic.

Mr. Brian Hoffman: Okay--.

Mr. Rich Montoni: --Next question please.

Operator: Next question is a follow up from the line of Brian Gisweli with Raymond James. Please go ahead with your question.

Mr. Brian Gisweli: Um, yeah, just a quick follow up - uh, you guys had taken, uh, Illinois out of the guidance, it looks like, as of December. Can you maybe talk a little bit about the union dynamics going on with this, uh, likelihood of appeal and, um, maybe also whether there would be termination costs attached to, uh, Illinois, uh, pending the contract relationship.

Mr. Rich Montoni: Sure, Brian. Ask, uh, Bruce Caswell to respond to that one.

Mr. Bruce Caswell: Happy to, Brian.

Um, as you know, uh, this was a two year contract, um, that--under which Maximus, and just by way of background, helps, uh, the state caseworkers verify the continued eligibility for, uh, individuals in the medical assistance programs including Medicaid.

Um, in July of 2012, um, the Union filed a grievance under their collective bargaining agreement that the state, uh, was required to use union employees. Um, June 20th, 2013, the arbitrator ruled, as you're aware, in favor of the union.

Um, and we're really awaiting further direction from our client regarding their intent to appeal. Uh, so I really can't speculate at this point.

Uh, they have, it's our understanding, until October to make that decision. Uh, so as a consequence, given the current, uh, environment, we've made, uh, the decision obviously to, um, reflect that contract as winding down in December, as would be required under the arbitrator's ruling.

Uh, that said, we'll continue to, um, seek guidance from our clients on what role, if any, uh, we might be able to continue to provide, uh, to help them effect a transition should they choose to go in that direction.

Uh, and I guess I would turn it over to Dave Walker to comment on, uh, the impact on any wind down costs or transition costs in their program.

Mr. David Walker: Uh, it's all gonna be very much tied to where we end up in the negotiation, but it's all baked into our forecast.

Mr. Brian Gisweli: Thanks a lot, guys.

Mr. Rich Montoni: And before we move on, uh, our next question, we did receive a query that I'd like to clarify, and it's really kind of a follow on to the earlier discussions as it relates to the operating margin in the human services segment. And to wrap up what Dave Walker shared with you, uh, while the operating margin for that segment was flat on a sequential basis, uh, we--and the main drivers were good performance by UK, good performance by Max Network with really, uh, the softness being what we've shared with you in the past, the domestic market, the US domestic market in human services.

That being said, we do expect that that segment will have, uh, growth and improvement in its operating margin in the fourth quarter, and we do expect that health will have another solid quarter. In fact, uh, I think we'll have top line and bottom line--uh, top line growth in both segments such that when you add it up, uh, we feel comfortable with our top line and bottom line guidance, adjusted EPS, uh, for fiscal '13.

Uh, in fact, at this point in time, we're confident that, uh, we tend to be at the upper end of both ranges.

So, with that, I'll open it up to any final questions that may be out there.

Mr. David Walker: For '13.

Mr. Rich Montoni: For '13, right.

Mr. David Walker: Yeah.

Operator: Thank you.

This concludes today's teleconference. You may disconnect your lines at this time, and thank you for your participation.

Slide: 1 SubTitle: David N. WalkerChief Financial Officer and TreasurerAugust 8, 2013 Title: Fiscal 2013 Third Quarter Earnings

Slide: 2 Title: Forward-looking Statements & Non-GAAP Information These slides should be read in conjunction with the Company’s most recent quarterly earnings press release, along with listening to or reading a transcript of the comments of Company management from the Company’s most recent quarterly earnings conference call.This document may contain non-GAAP financial information. Management uses this information in its internal analysis of results and believes that this information may be informative to investors in gauging the quality of our financial performance, identifying trends in our results, and providing meaningful period-to-period comparisons. These measures should be used in conjunction with, rather than instead of, their comparable GAAP measures. For a reconciliation of non-GAAP measures to the comparable GAAP measures presented in this document, see the Company’s most recent quarterly earnings press release.A number of statements being made today will be forward-looking in nature. Such statements are only predictions and actual events or results may differ materially as a result of risks we face, including those discussed in our SEC filings. We encourage you to review the summary of these risks in Exhibit 99.1 to our most recent Form 10-K filed with the SEC. The Company does not assume any obligation to revise or update these forward-looking statements to reflect subsequent events or circumstances.

Slide: 3 Title: Total Company Financial Results Another quarter of strong growthQ3 FY13 revenue increased 26% to $334.3M compared to $266.4M last year, which included a $10.2M change order in the Health Segment that bolstered revenue and operating margins last yearSubstantially all of the revenue growth in Q3 was organic, driven by solid momentum from both business segments and revenue expansion from domestic and international operationsAccretive revenue growth in Q3 helped drive higher operating income and margins; for Q3, total Company operating income, excluding legal, settlement and acquisition expense, increased 30% to $45.4M (13.6% operating margin) compared to last year Earnings were in-line with our expectations; Q3 income from continuing operations, net of taxes, totaled $28.0 million ($0.40 per diluted share) GAAP diluted EPS included $0.01 of net legal, settlement and acquisition expense; excluding this, adjusted diluted EPS for Q3 increased 32% to $0.41 per share *Excluding legal, settlement and acquisition expense Note: numbers may not add due to rounding

Slide: 4 Title: Health Services Segment Revenue Q3 revenue increased 28% to $217.9 million compared to the same period last year, driven by favorable volumes in our health appeals business, organic growth from new work, and the expansion of existing programs.Operating Income & MarginsQ3 operating income increased 34% to $34.4 million compared to the same period last year and operating margin improved to 15.8% in Q3, driven by accretive growth in our federal appeals and other transaction-based programs. This compares favorably to 15.1% reported in the prior-year period, which benefited from the aforementioned $10.2 million change order that accounted for approximately $0.05 to overall earnings in Q3 of last year. Demand for Core Services Remains StrongThe Health Services Segment continues to benefit from strong demand in our core service areas. Since our last call, we’ve announced new health insurance exchange wins in Maryland, Hawaii and the District of Columbia.This expands our footprint for customer contact centers to six state exchanges and the federal exchange.

Slide: 5 Title: Human Services Segment RevenueQ3 revenue increased 21% to $116.4 million compared to the same period last year, driven principally by the ongoing ramp-up of the Work Programme contract in the UK, as well as growth from our other international operations. Operating Income & MarginsQ3 operating income grew 20% and totaled $11.0 million with an operating margin of 9.5%. This compares to operating income of $9.2 million and a margin of 9.6% last year. The prior-year period included a $2.1 million net benefit from a fixed-price contract. Excluding the net benefit, the Segment had solid year-over-year operating margin expansion, driven by the ongoing ramp up in the UK, and accretive growth in other operations outside the U.S. that offset the expected lower margin in Australia.

Slide: 6 Title: Balance Sheet and Cash Flows Cash Flows & DSOsCash provided by operating activities from continuing operations totaled $49.7M and free cash flow totaled $32.7M at 6/30Solid cash flow driven by strong earnings and timing related to working capital itemsAs mentioned in Q2, experienced some payment slowdowns in 1H FY13. Some payments received in Q3 DSOs were 65 days at June 30, 2013 and expect further collection progress in Q4 Cash Usage and Cash BalancesUsed cash of approximately $12.4M to repurchase the equivalent of 329,800 shares of MMS stock At June 30, $102.2M available for future repurchasesCash balance unfavorably impacted by currency, which decreased cash balance by approximately $14.6M in Q3At June 30, cash and cash equivalents of $187.9M and approximately $142M of this cash was held overseasSubsequent to quarter close, we used international cash of approximately $71.4 million to complete the HML acquisitionWe remain very focused on sensible cash deployment and using cash to drive long-term shareholder value. Our priorities include: 1) quarterly cash dividend, 2) opportunistic share repurchases, 3) strategic acquisitions, and 4) the ongoing funding of organic growth. Reconciliation to Free Cash Flow Note: numbers may not add due to rounding

Slide: 7 Title: Guidance Reiterating 2013 Revenue and Earnings Guidance; Maintaining Cash Flow GuidanceReiterating 2014 Revenue and Earnings Preliminary GuidanceDynamics shaping our FY 14 guidance include: Full-year benefit in FY 14 from new programs that provided partial-year contributions in FY13 (examples: California worker’s compensation and new health insurance exchange contracts)Solid top-line growth in the federal market with contracts that are often lower-margin, cost-reimbursable work; also expect our appeals volumes to return to more normalized levels as we move into next yearExpected reduction in our guidance, which includes non-recurring HIX work in states like MN and CA and contracts that served as bridge programs to the Affordable Care Act, such as work related to pre-existing conditions provisions, that are now folding into state exchange operationsProgram changes, including the sizeable reduction in revenue and profit from the California Healthy Families CHIP program, which has been rolled into the Medicaid program; expect continued revenue and profit decline moving into FY 14IL Medicaid eligibility verification contract is at risk due to an arbitrator’s ruling that the state is required to use state employees to perform this work; our FY 14 model assumes that the program winds down by the end of December 2013Forecasted our FY14 tax rate of 37% reflecting international mix of business and favorable legislative changes outside of U.S.When you add it all up, we manage a portfolio of contracts with normal fluctuations that are more than offset by growth.

Slide: 8 SubTitle: Richard A. MontoniPresident and Chief Executive Officer August 8, 2013 Title: Fiscal 2013 Third Quarter Earnings

Slide: 9 Title: Solid Financial Results Set Growth Platform for FY14 Quarterly financial results right in-line with our growth trajectory for the remainder of fiscal 2013 Results set a solid platform for continued top- and bottom-line growth next fiscal year Targeting double digit growth for fiscal 2014, as we continue to benefit from macro drivers and solid demand trends in core markets

Slide: 10 Title: Exceeded Initial Goal for Health Insurance Exchanges Successfully established the leading position in the state-based health insurance exchange market Operating the customer contact centers for six of the sixteen state-based exchanges: CT, DC, HI, MD, NY and VTAlso part of team selected for the contact center operations of the federal marketplaceAll of this new work adds up to more than $150 million in new annual contract value This exceeds the target goal that we laid out of winning 20% to 25% of the total addressable market of $500 million in new annual contract value Pleased to have secured fair share (and a little bit more) of HIX work

Slide: 11 Title: Health Insurance Exchange Operations Ramping Nicely MD HIX customer contact center went live last week; our professionals are answering general inquiries about the Affordable Care Act and health insurance exchange, as well as helping consumers prepare for the open enrollment period that commences on October 1Federal marketplace operations in Texas launched last week; customer service representatives are taking callsBuild out of our second federal site in Idaho progressing as planned; team will be ready for open enrollment in October Build out of remaining HIX contracts on track; hiring progressing as expected; training teams gearing up to prepare customer service representatives for incoming calls

Slide: 12 Title: Health Care Reform Remains Long-Term Growth Driver Will be operations-ready to support our government clients for the October 1 open enrollment Will also continue to assist our current state clients who are defaulting to the federal marketplace as they strive to meet ACA requirements, including “no wrong door” provisionsWith new exchange operations on track, remain keenly focused on the next wave of ACA-related opportunities Over the next several years many states will likely consider additional initiatives, including the expansion of Medicaid and other health provisions under ACA As we’ve stated all along, health care reform will be a long-term, multi-year growth driver for MAXIMUS, particularly as the different health insurance marketplaces evolve over time

Slide: 13 Title: Acquired UK’s Largest Occupational Health Provider Acquisition of Health Management important next step for introducing core health offerings to the UK Largest independent occupational health provider in the UK; services include: Health Assessments Sickness Absence Referrals & Management Services Wellness Programs Primary Care & Well-being Services Employee Assistance ProgramsBrings a team of recognized and highly qualified occupational health consultants to MAXIMUS Great fit because both companies share many of the same fundamental values; both keenly focused on providing clients with innovative solutions to address health, social and productivity challenges

Slide: 14 By coupling our core independent review competencies developed in the U.S. with an established, proven partner in the UK, created an exceptionally strong delivery team that is well positioned for future opportunities Acquisition of Health Management demonstrates our commitment to serving more clients in this important market and working with UK government to achieve program goalsContinue to see emerging opportunities that may lead to RFP activity during fiscal 2014; very excited to further enhance offerings in existing markets to create new, long-term growth platforms Title: Health Management Acquisition Enhances UK Portfolio

Slide: 15 Title: Update on Work Programme in the UK Expansion in the UK builds upon the positive reputation and solid performance by welfare-to-work team; remain one of the top performing vendors under the Work Programme, a position most recently highlighted in vendor statistics issued in late June Since we started contract in July 2011, referrals into the Work Programme have been lumpy As we’ve gained additional experience on the program, achieved confirming data points that provide better trend data, improve overall visibility, and allow us to refine our operational and financial models As disclosed in fiscal 2012, initially saw higher caseload volumes However, since the start of Program Year Two in April 2012, experienced overall referrals lower than forecasts initially laid out Initially thought volumes would return to more normalized levels, based on previous experience where case volumes varied widely month to monthVolumes remained lower than expected, which led to lower revenue levelsManaged resources and labor and the contract remains in-line with net income expectationsFactored into current fiscal 2013 guidance, as well as preliminary guidance for fiscal 2014

Slide: 16 Title: Future Reallocation Models for Work Programme Intra-region reallocation: shift in caseloads within regions we already operateDepartment for Work and Pensions stated intra-region reallocations would only shift up to 5% of caseloads to other qualified vendors within that region Shift is immaterial to MAXIMUS: less than $500,000 in new annual revenue in the regions we currently serve Inter-region reallocation: qualified, high-performing vendors can pick up entirely new region as long as they are on the framework for that particular region Unclear what the timing on this reallocation will be; don’t believe there will be a material, near-term reallocation of workOur interest in picking up new regions is contingent upon overall terms and conditions of the contract While reallocation opportunities are an important part of our land and expand strategy, we are far more excited about the many new promising opportunities starting to materialize for new programs and new work in the UKCurrent operations combined with acquisition of Health Management create springboard for many of those longer-term, greenfield opportunities

Slide: 17 Title: Achieved Rebid Goal for Fiscal 2013 Had 14 contracts with a total value of approx. $475 million up for rebid in fiscal 13 Secured $440 million to date; met our goal to win 90%+ of the total contract value up for rebid Rebid on our Texas Medicaid contract still being negotiated; current contract ends in August and we expect finalization very soon Now have one rebid remaining with a total contract value of approximately $11 million All considered, fiscal 2013 is tracking to be a very successful year for rebidsWill provide information about contracts up for rebid in fiscal 2014 on our November call, but expect it to be a light year from a rebid perspective

Slide: 18 Title: New Awards and Sales Pipeline Delivered another solid quarter of new sales awards, with $1.3 billion of year-to-date signed awardsNew contracts pending contributed an additional $413 million to our sales awardsThese are contracts where we’ve received notification of award and are in contract negotiations, but have not yet been signedSales pipeline of $2.2 billion, slightly lower than the previous quarterMostly due to contracts shifting out of the pipeline and into the award categories, but also the loss of a federal eligibility support contractPipeline includes opportunities across multiple geographies and both segments

Slide: 19 Title: Meaningful Progress Towards Long-Term Objectives Continue to make steady, meaningful progress towards our three-prong, long-term growth strategy:Securing our fair share of health care reform work in the U.S.Growing our federal book of businessExpanding our international operationsProud of achievement of securing fair share of first wave of HIX contracts; remain optimistic about other long-term opportunitiesAcquisition of Health Management creates strengthened position for future opportunities in the UK health market and supports international growth objectivesLong-term growth is not dependent on a single business area or geography, but upon macro trends and extended growth drivers; see many new emerging opportunities for our core capabilities in all our geographiesWith our fiscal 2014 preliminary guidance in place, we remain committed to generating long-term shareholder value as we continue to grow the business