|

|

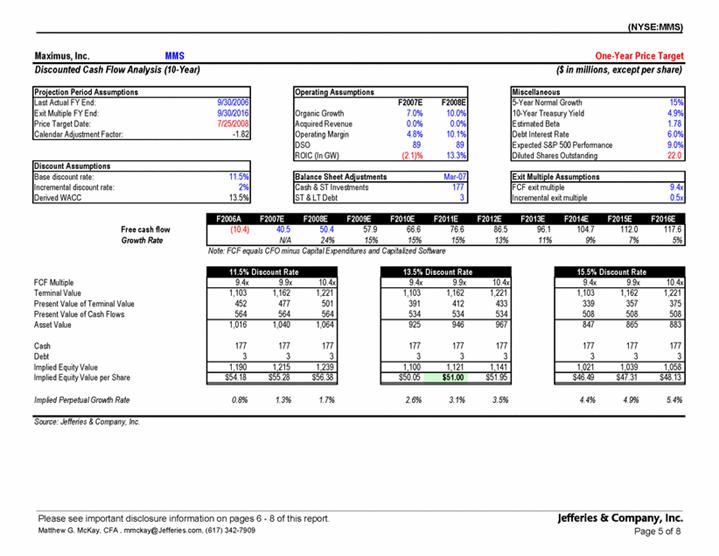

Page 8 Stifel,

Nicolaus and Company, Inc. Maximus, Inc. Balance Sheet and Cash Flow ($ in

thousands) FY ends September 30 Balance Sheet FY07 1Q08 2Q08 3Q08 4Q08 FY08

1Q09 2Q09 3Q09 4Q09E FY09E 1Q10E 2Q10E 3Q10E 4Q10E FY10E FY11E Cash and

short-term investments 62,654 $ 63,747 $ 78,271 $ 120,957 $ 64,004 $ 87,539 $ 95,368 $ 95,719 $ 101,375 $ 108,146 $ 115,278 $ 117,568 $ Accounts

receivable, net 119,267 122,692 126,793 128,819 101,876 96,350 116,884

124,829 108,892 114,348 124,452 128,730 Unbilled receivables 49,771 52,314

49,721 30,695 28,180 35,388 30,290 37,894 30,069 35,147 28,885 39,789 Prepaid

and other current assets 7,688 15,719 11,649 10,215 12,321 35,730 27,547

27,547 27,547 27,547 27,547 27,547 Deferred taxes 11,267 9,490 10,255 25,750

40,029 8,735 12,695 12,695 12,695 12,695 12,695 12,695 Total current assets

250,647 263,962 276,689 316,436 246,410 263,742 282,784 298,684 280,578

297,883 308,857 326,329 Property, plant and equipment, net 35,580 34,333

33,799 33,994 33,392 33,549 37,845 41,044 43,028 45,062 47,353 49,799 Net

Software Development Costs 29,306 29,183 29,714 14,125 14,362 16,681 17,201

17,201 17,201 17,201 17,201 17,201 Deferred contract costs 7,712 6,273 5,435

5,324 6,384 7,604 8,530 8,530 8,530 8,530 8,530 8,530 Deferred taxes - - - 10,933

3,217 1,440 - - - - - - Other assets 92,833 92,518 91,326 69,483 66,303

65,007 66,817 66,817 66,817 66,817 66,817 66,817 Total assets 416,078 426,269

436,963 450,295 370,068 388,023 413,177 432,276 416,154 435,493 448,758

468,676 Current liabilities: Accounts payable 52,441 53,391 51,802 48,950

36,799 53,218 49,971 53,042 37,855 50,572 51,135 55,694 Accrued compensation

and benefits 25,771 28,390 29,417 26,684 22,681 24,932 26,830 33,397 24,504

24,469 28,097 35,067 Billings in excess of costs and estimated earnings

37,461 33,151 33,836 19,676 21,441 19,351 21,824 23,636 25,622 25,890 27,258

27,158 Notes payable & other (cap. lease obligations) 1,643 1,238 830 417

- - - - - - - - Income taxes payable - - - 4,011 - - - - - - - - Deferred

taxes 2,675 998 1,237 64,919 24,202 19,435 20,262 20,262 20,262 20,262 20,262

20,262 S corporation distribution payable - - - - - - - - - - - - Total

current liabilities 119,991 117,168 117,122 164,657 105,123 116,936 118,887

130,337 108,242 121,193 126,751 138,181 Long-term debt - - - - - - - - - - -

- Deferred taxes 11,202 12,752 11,810 1,617 1,668 1,573 2,212 2,212 2,212

2,212 2,212 2,212 Other liabilities 12,319 11,470 10,996 8,315 6,861 7,884

8,972 8,972 8,972 8,972 8,972 8,972 Total liabilities 143,512 141,390 139,928

174,589 113,652 126,393 130,071 141,521 119,426 132,377 137,935 149,365

Redeemable common stock - - - - - - - - - - - - Common stock - - - - - - - -

- - - - Additional paid-in capital 31,976 36,514 39,130 39,220 18,496 11,542

20,138 14,728 9,318 3,908 (1,502) (6,912) Retained earnings 240,590 248,365

257,905 236,486 237,920 250,088 262,968 276,026 287,410 299,208 312,325

326,223 Total stockholders' equity 272,566 284,879 297,035 275,706 256,416

261,630 283,106 290,754 296,728 303,116 310,823 319,311 Total liab &

stockholders' equity 416,078 426,269 436,963 450,295 370,068 388,023 413,177

432,276 416,154 435,493 448,758 468,676 15.9% Cash Flow Statement FY07 1Q08

2Q08 3Q08 4Q08 FY08 1Q09 2Q09 3Q09 4Q09E FY09E 1Q10E 2Q10E 3Q10E 4Q10E FY10E

FY11E Cash flows from operating activities Net income$ (8,255) $ 10,605 $ 9,627 $ 11,405 $ (24,960) $ 6,677 $ 11,963 $ 11,027 $ 14,983 $ 14,029 $ 52,002 $ 12,341 $ 12,744 $ 14,049 $ 14,817 $ 53,951 $ 58,633 Deferred taxes

4,195 3,327 (1,707) (26,015) 12,043 10,616 (309) - - - - - Depreciation and

amortization 5,039 4,799 4,271 (1,581) 2,746 2,982 2,820 2,820 2,820 2,820

2,820 2,820 Other 3,600 2,154 (4,588) 33,370 2,051 2,472 1,834 800 800 800

800 800 Funds from operations 23,439 19,907 9,381 (19,186) 28,803 27,097

19,328 17,649 15,961 16,364 17,669 18,437 (Increase) decrease in A/R 13,695

(3,425) (4,101) (2,026) 26,943 5,526 (20,534) (7,945) 15,937 (5,456) (10,104)

(4,278) (Increase) decrease in excess costs and earnings (7,571) (2,543)

2,593 19,026 2,515 (7,208) 5,098 (7,604) 7,826 (5,078) 6,261 (10,904)

(Increase) decrease in prepaid other c/a 1,471 (8,031) 4,070 1,434 (2,106)

(23,409) 8,183 - - - - - (Increase) decrease in other assets - - - - - - - -

- - - - Increase (decrease) in compensation (3,678) 2,619 1,027 (2,733) (4,003)

2,251 1,898 6,567 (8,893) (34) 3,627 6,970 Increase (decrease) in A/P (1,984)

950 (1,589) (2,852) (12,151) 16,419 (3,247) 3,071 (15,188) 12,717 563 4,560

Increase (decrease) in income tax payable - - - 4,011 (4,011) - - - - - - -

Increase (decrease) in excess billings (680) (2,871) 1,523 (14,049) 705

(3,310) 1,547 1,812 1,986 268 1,368 (100) Increase (decrease) in other

liabilities 2,176 (849) (474) (2,681) (1,454) 1,023 1,088 - - - - - Other

changes to working capital (plug) (6,079) (1,253) 369 37,537 (62,418) 20,472

(1,560) - - - - - Working capital changes (2,650) (15,403) 3,418 37,667

(55,980) 11,764 (7,527) (4,099) 1,668 2,417 1,716 (3,752) Net cash provided

by operating activities 51,190 20,789 4,504 12,799 18,481 56,573 (27,177)

38,861 11,801 13,550 37,035 17,629 18,780 19,385 14,686 70,480 73,589 Capital

expenditures, net (17,893) (4,083) (3,055) (6,730) (1,581) (15,449) (4,142)

(5,448) (6,033) (6,019) (21,642) (4,804) (4,854) (5,111) (5,266) (20,036)

(21,217) % of revenue 2.4% 2.0% 1.5% 3.3% 0.8% 1.9% 2.3% 3.0% 3.3% 3.0% 2.9%

2.5% 2.5% 2.5% 2.5% 2.5% 2.5% Acquisitions - - 10,572 29,885 - - - - - - - -

Other investing activities (plug) - - 59 (2,815) (1,667) 282 3,710 - - - - -

Net cash used by investing activities (4,083) (3,053) 3,901 25,489 (5,809)

(5,166) (2,323) (6,019) (4,804) (4,854) (5,111) (5,266) Free Cash Flow

(excluding acquisitions) 33,297 16,706 1,449 6,069 16,900 41,124 (31,319)

33,413 5,768 7,532 15,394 12,825 13,926 14,274 9,420 50,444 52,372 % of net

income -403.4% 145.4% 29.3% 93.5% 89.3% Increase (decrease) in debt (401)

(404) (408) (414) (417) - - - - - - - Increase (decrease) in equity (148,733)

2,195 97 990 (21,785) (8,071) 452 (5,410) (5,410) (5,410) (5,410) (5,410)

Other financing activities (incl. dividend) (1,925) (2,149) (1,865) (1,860)

(1,765) (2,089) (2,101) (1,771) (1,758) (1,745) (1,732) (1,719) Net cash

provided from financing activities (151,059) (358) (2,176) (1,284) (23,967)

(10,160) (1,649) (7,181) (7,168) (7,155) (7,142) (7,129) Net increase

(decrease) in cash and cash equivalents 38,635 (134,353) 1,093 14,524 42,686

(76,050) (56,953) 23,535 7,829 351 (25,238) 5,657 6,771 7,132 2,290 21,849

45,444 Source: Maximus, Inc. and Stifel Nicolaus estimates George A. Price,

Jr. (443) 224-1323 gaprice@stifel.com 8/6/2009 Shlomo H. Rosenbaum (443)

224-1322 shrosenbaum@stifel.com Richard M. Eskelsen (443) 224-1366

eskelsenr@stifel.com Maximus, Inc. (MMS) August 7, 2009

|