Use these links to rapidly review the document

TABLE OF CONTENTS

FINANCIAL STATEMENTS

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended September 30, 2013

Commission file number: 1-12997

MAXIMUS, INC.

(Exact name of registrant as specified in its charter)

| Virginia (State or other jurisdiction of incorporation or organization) |

54-1000588 (I.R.S. Employer Identification No.) |

|

1891 Metro Center Drive, Reston, Virginia (Address of principal executive offices) |

20190 (Zip Code) |

Registrant's telephone number, including area code: (703) 251-8500

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

|---|---|---|

| Common Stock, no par value | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of "accelerated filer and large accelerated filer" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

The aggregate market value of outstanding voting stock held by non-affiliates of the registrant as of March 31, 2013 was $2,639,737,871 based on the last reported sale price of the registrant's Common Stock on The New York Stock Exchange as of the close of business on that day.

There were 68,538,100 shares of the registrant's Common Stock outstanding as of November 1, 2013.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive Proxy Statement for its 2014 Annual Meeting of Shareholders to be held on March 19, 2014, which definitive Proxy Statement will be filed with the Securities and Exchange Commission not later than 120 days after the end of the registrant's fiscal year, are incorporated by reference into Part III of this Form 10-K.

MAXIMUS, Inc.

Form 10-K

September 30, 2013

Table of Contents

2

SPECIAL NOTE REGARDING FORWARD LOOKING STATEMENTS

Included in this Annual Report on Form 10-K are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These forward-looking statements are based on current expectations, estimates, forecasts and projections about our company, the industry in which we operate and other matters, as well as management's beliefs and assumptions and other statements that are not historical facts. Words such as "anticipate," "believe," "could," "expect," "estimate," "intend," "may," "opportunity," "plan," "potential," "project," "should," "will" and similar expressions are intended to identify forward-looking statements and convey uncertainty of future events or outcomes. These statements are not guarantees and involve risks, uncertainties and assumptions that are difficult to predict. Actual outcomes and results may differ materially from such forward- looking statements due to a number of factors, including without limitation:

As a result of these and other factors, our past financial performance should not be relied on as an indication of future performance. Additionally, we caution investors not to place undue reliance on any forward-looking statements as these statements speak only as of the date when made. Except as otherwise required by law, we undertake no obligation to publicly update or revise any forward-looking statements, whether resulting from new information, future events or otherwise.

3

Throughout this annual report, the terms "MAXIMUS," "Company," "we," "our" and "us" refer to MAXIMUS, Inc. and its subsidiaries. A list of key terms is included in a glossary at the end of this section.

General

We provide business process services ("BPS") to government health and human services agencies under our mission of Helping Government Serve the People.® We are one of the largest pure-play health and human services administrative providers to governments in the United States, Australia, Canada, the United Kingdom and Saudi Arabia. We use our expertise, experience and advanced technological solutions to help government agencies run efficient, cost-effective programs and to improve program accountability and outcomes, while enhancing the quality of services provided to program beneficiaries.

Over the course of the past five years, our revenue and earnings have grown primarily as a result of economic, demographic and legislative trends, which are driving demand for services from providers, such as MAXIMUS, who can provide efficient, cost-effective solutions to problems, such as:

With our proven track record and expertise, we are in a superior position to provide these services. We believe that we can bring the right combination of people, business process and technology to deliver the best value solution to governments. This has allowed us to gain market share in an area that has significant barriers to entry. As a result, we are:

We pursue selective acquisitions to enhance and expand our offerings or geographic presence. In 2013, we acquired Health Management Limited, the leading provider of independent medical assessments in the United Kingdom; in 2012, we acquired Policy Studies, Inc., a provider of health and human services operations in the United States; and in 2010, we acquired DeltaWare Services, Inc., a provider of software in Canada.

Much of our revenues are derived from long-term contractual arrangements with governments. Base contracts are typically three to five years and often have additional option periods, which provide good visibility in terms of predicting revenues. Most of our contracts are related to programs that are long-term in nature, such as Medicaid and Medicare. Our client relationships are frequently decades long.

4

Our business segments

Our reportable segments are Health Services and Human Services. For more information concerning our segment presentation, including comparative revenue, gross profit, operating profit, identifiable assets and related financial information for the 2013, 2012 and 2011 fiscal years, see "Note 2. Business segments" within Item 8 of this Form 10-K, which we incorporate by reference here.

Health Services Segment

Our Health Services Segment generated 65% of our total revenue in fiscal year 2013. This segment provides a variety of business process services, as well as related consulting services, for state, provincial and federal government programs, including Medicaid, CHIP, SNAP (Supplemental Nutrition Assistance Program), Medicare, the Affordable Care Act and Health Insurance BC (British Columbia). The segment's services help improve the efficiency, cost effectiveness, quality and accountability of government-sponsored health benefit programs. In this segment, our BPS and consulting services can be described as follows:

Historically, the Health Services business has not been subject to significant effects from seasonality; however it experiences revenue and margin fluctuations due to transaction-based work, such as periodic program open enrollment and activity related to contract life cycles. During the first quarter of our fiscal year, reductions in working days due to holidays and vacations may impact our sales and accounts receivable, but the effect is generally not significant. In the future, the segment may experience more seasonality related to ACA which provides for a six month open enrollment in the first year and a three month open enrollment in subsequent years.

Human Services Segment

Our Human Services Segment generated 35% of our total revenue in fiscal year 2013. This segment provides federal, national, state and county human services agencies with a variety of business process services, as well as related consulting services for welfare-to-work, child support, higher education and K-12 special education programs. Our services can be described as follows:

5

transition from government assistance programs to sustainable employment and economic independence;

The Human Services Segment may experience some seasonality due to holidays and vacations. In addition, the segment typically derives revenue and associated higher margins from our tax credit business in the second half of the year, principally in the fourth quarter.

Geographic Information

We operate in the United States, Australia, Canada, the United Kingdom and Saudi Arabia. The distribution of revenues and assets among the United States, Australia and the rest of the world are included in "Note 2. Business Segments" within Item 8 of this Form 10-K.

Market overview

We expect that demand for our core health and human services offerings will continue to increase over the next few years, driven by new legislation, austerity measures and increasing caseloads, as governments strive to deliver more services with fewer resources. Legislation, such as the Affordable Care Act (ACA) in the United States as well as other health and welfare reform initiatives abroad, has created increased demand for our services, a trend we expect to continue over the next several years. We believe that we remain well-positioned to benefit from this increasing demand as governments look for ways to improve overall program efficiency and achieve value for funds spent on social benefits programs.

Demand for our services is contingent upon factors that affect governments, including:

As a result, governments utilize BPS companies, such as MAXIMUS, to help them deliver innovative, efficient and cost-effective services to beneficiaries on their behalf. We possess the knowledge and resources to operate government health and human programs efficiently, while maintaining the service levels demanded by our government clients. With the ability to tightly balance resources with demand, we also offer the flexibility and scalability that governments do not always possess.

6

Health Services Market Environment

Over the past decade, health care costs have risen substantially in the United States, a trend that is expected to continue. U.S. health care spending, among the highest of all industrialized countries, is increasing at a rate that outpaces inflation and national income growth. Stemming these costs, as well as improving quality and access to health care, is a major policy priority for governments.

In recent years, state fiscal realities have prompted states to reexamine their Medicaid programs. Many states have made program changes, most notably through benefit changes and the expansion of managed care to new populations—including the aged, blind and disabled (ABD) populations—that have historically been served through fee-for-service Medicaid. Although ABD populations represent only a quarter of the total Medicaid population, they are responsible for approximately 70% of the costs. We have seen growth in our current programs from Medicaid managed care expansion. We believe that we remain well-positioned to benefit from future Medicaid managed care expansion due to our role as the administrative enrollment vendor for 19 Medicaid managed care programs.

In March 2010, Congress passed ACA, a comprehensive overhaul of the U.S. health insurance system that initially seeks to expand access to health care, while ultimately improving quality and reducing overall delivery costs. Most notably, ACA aims to expand health insurance coverage to more than 30 million Americans through Medicaid expansion and subsidized insurance coverage purchased through health insurance exchanges. In June 2012, the U.S. Supreme Court ruled that Medicaid expansion under ACA was optional for states. Nevertheless, the Congressional Budget Office estimates that most states will expand Medicaid coverage over the next several years. The ACA also extends CHIP through 2019, provides increased matching federal funds, and guarantees funding through 2015. We currently serve as the administrative vendor for CHIP in nine states.

The law also promotes the integration of new health insurance exchanges with existing state Medicaid and CHIP programs to provide a "no wrong door" entry for program beneficiaries. A health insurance exchange is designed to be an insurance marketplace where individuals and small businesses can shop, compare and buy affordable and qualified health benefit plans. Under the ACA, states were able to determine how they wanted to create their health insurance exchanges by either relying upon the federal exchange or creating their own exchange. In 2013, approximately 35 states opted to use the federal exchange and the remaining states, plus the District of Columbia, chose to operate their own state-based exchanges. States currently on the federal exchange may transition to their own state-based exchanges in the future. Many of the core functions of a health insurance marketplace are similar to Medicaid and CHIP, including consumer outreach and education, eligibility and enrollment, customer contact centers, web portals, and comprehensive business process managed services to help beneficiaries navigate the new exchanges and enroll in health insurance plans. As a result, we are operating customer contact centers for the District of Columbia, five state-based exchanges and two customer contact centers as a subcontractor for the federal exchange.

ACA also includes enhanced consumer protections for health insurance appeals. The law requires an independent, evidence-based external review process and the option for individuals to appeal coverage determinations or claims to insurance companies. This expands the requirement to states that do not have an existing compliant external review process and non-governmental, self-insured plans which previously were not required to have an objective independent health appeals process. We are one of the largest providers of evidence-based health insurance appeals to Medicare and more than 30 state agencies.

We believe the current health environment positions us to benefit from continued demand under the ACA. Overall, we expect the underlying demand for our services to increase over the next several years as states consider transitioning from the federal exchange to their own state-based exchanges and as additional states contemplate Medicaid expansion. In September 2013, the Centers for Medicaid and Medicare awarded MAXIMUS a contract to provide the overall management of the eligibility appeals

7

process for the federal exchange. This one year, $43.2 million contract has four one-year option periods that would bring the total contract value to $383.2 million if all option periods and optional tasks are exercised.

Human Services Market Environment

The Human Services market has experienced increased demand driven by the need for governments to reduce costs and improve efficiency of social benefits programs. The most dynamic portion of the market is in the welfare-to-work arena where governments worldwide are seeking to reform their programs as an important component of comprehensive fiscal austerity measures. Certain governments are modeling new welfare reforms after established programs in Australia and the United States. Variations of these models, with which we have a substantial amount of experience, knowledge and expertise, are being emulated around the world through privatized efforts, with MAXIMUS being a leading provider.

We believe we are well-positioned to compete for these global welfare-to-work opportunities because of our established presence, strong brand recognition, and ability to achieve the requisite performance requirements and outcomes outlined in the new reform measures. We offer clients demonstrated results and more than 20 years of proven experience in administering welfare-to-work programs in several states and countries.

Since 1997, we have provided comprehensive welfare-to-work case management services throughout the United States. In Australia, we are one of the largest and highest rated welfare-to-work providers where we operate more than 80 sites and 65 outreach locations. We also have an established presence in the United Kingdom's welfare-to-work market and presently provide employment and job training services under the country's ambitious reform effort called the Work Programme. This program is a key component of the coalition government's austerity plan to rein in costly benefits programs and reduce mounting debt. The Work Programme consolidates many of the U.K.'s disparate welfare-to-work programs into a single, back-to-work effort. In fiscal 2012, we expanded our geographic reach in the welfare-to-work market with new programs in Canada and Saudi Arabia.

In addition to welfare reform, we have seen an increase in initiatives to use private firms for children's services, such as family maintenance and child support. We currently provide services to the Family Maintenance Enforcement Program in British Columbia as well as several jurisdictions throughout the United States, including Shelby County, Tennessee and Baltimore, Maryland, two of the largest child support privatization efforts in the nation.

We believe ongoing reform initiatives, as well as measures to reduce costs and improve efficiencies, combined with our outstanding performance, expertise and proven solutions will continue to drive demand for our core human services business across multiple geographies.

Our growth strategy

Our goal is to enable future growth by remaining a leading provider of operations program management and consulting services to government agencies. The key components of our business growth strategy include the following:

Pursue new domestic and international business opportunities and expand our customer base. With more than 35 years of business expertise in the government market, we continue to be a leader in developing innovative solutions to meet the evolving needs of government agencies. We seek to grow our domestic and international businesses by leveraging our existing core capabilities, consistently delivering the required outcomes for governments to achieve program goals, and pursuing opportunities with new and current clients.

8

Grow long-term, recurring revenue streams. We seek to enter into long-term relationships with clients to meet their ongoing objectives. As a result, long-term contracts (three to five years with additional option years) are often the preferred method of delivery for customers and are also beneficial to us. We believe an incumbent has a considerable advantage in recompetes and that customer relationships can last decades.

Pursue strategic acquisitions. We will selectively identify and pursue strategic acquisitions. Acquisitions can provide us with a rapid, cost-effective method to enhance our services, obtain additional skill sets, expand our customer base, cross-sell additional services, enhance our technical capabilities, and establish or expand our geographic presence.

Continue to optimize our current operations to drive innovation and quality to customers. We continue to seek efficiencies and optimize operations in order to achieve sustainable, profitable growth. We will continue to deliver quality business process services to clients to improve cost effectiveness, program efficiency and overall program scalability as governments deal with rising demand and increasing caseloads.

Recruit and retain highly skilled professionals. We continually strive to recruit motivated individuals, including top managers from larger organizations, former government officials, consultants experienced in our service areas and recent college graduates with degrees aligned with our mission, such as degrees in government policy and administration. We believe we can continue to attract and retain experienced and educated personnel by capitalizing on our focused market approach and our reputation as a premier government services provider.

Focus on core health and human services business lines. We have centered our core business offerings on delivering business process managed services to government health and human services agencies. Our market focus and established presence positions us to benefit from health care reform in the United States and welfare reform initiatives abroad.

See Exhibit 99.1 of this Annual Report on Form 10-K under the caption "Special Considerations and Risk Factors" for information on risks and uncertainties that could affect our business growth strategy.

Competitive advantages

We offer a private sector alternative for the operation and management of critical government-funded health and human services programs. Our reputation and extensive experience over the last 38 years give us a competitive advantage as governments value the level of expertise, proven delivery and brand recognition that we bring our customers. The following are the competitive advantages that allow us to capitalize on various market opportunities:

Proven track record, ability to deliver outcomes and exceptional brand recognition. Since 1975, we have successfully assisted governments in delivering cost-effective services to beneficiaries of government programs. We operate large-scale program management operations on behalf of government agencies, improving the quality of services provided to beneficiaries, and achieving the necessary outcomes to help these governments cost-effectively meet their program goals. This has further enhanced our brand recognition as a proven partner with government agencies.

Subject matter expertise. Our workforce includes many individuals who possess substantial subject matter expertise in areas critical to the successful design, implementation, administration and operation of government health and human services programs. Many of our employees have worked for governments in management positions and can offer insights into how we can best provide valuable, practical and effective services to our clients.

9

Intellectual property that supports the administration of government programs. We have proprietary solutions to address client requirements in our market that are configurable or provide a platform that can be transferred to meet contractual needs. We also leverage commercial off-the-shelf platforms across multiple contracts in which we have considerable expertise to ensure we can deploy repeatable proven solutions. The Company also leverages software development methodology to shorten software development cycles. Extensive use of shared infrastructure and standard solutions provides considerable price and quality advantages. Management believes our extensive industry focus and expertise embedded in our systems and process provide us with a competitive advantage.

Flexibility and Scalability. We are experienced in launching large scale operations under compressed time frames. We offer clients the flexibility and scalability to deliver the people, processes and technology to complete short- and long-term contractual assignments in the most efficient and cost-effective manner.

Financial strength. We maintain a strong balance sheet, generate consistent annual cash flow, and have minimal long-term debt. We possess the financial strength to ensure clients can confidently trust MAXIMUS to safely operate their high-profile public health and human services programs.

Focused portfolio of services. We are one of the largest publicly traded companies that provide a portfolio of BPS health and human services specifically to government customers. Our government program expertise and proven ability to deliver defined, measurable outcomes differentiate us from other firms and non-profit organizations with limited resources and skill sets, as well as from large consulting firms that serve multiple industries and lack the focus necessary to manage the complexities of serving health and human services government agencies efficiently.

Established international presence. International governments are seeking to improve government-sponsored health and human services programs and contain costs. We have an established presence in Australia, Canada, the United Kingdom and Saudi Arabia. Our international efforts are focused on delivering cost effective welfare-to-work and health insurance eligibility and enrollment services to beneficiaries on behalf of governments.

Expertise in competitive bidding. Government agencies typically award contracts through a comprehensive, complex and competitive requests for proposals (RFPs) and bidding process. Although the bidding criteria varies from contract to contract, we believe that typical contracts are awarded based upon a mix of technical solution and price. In some cases, governments award points for past performance tied to program outcomes. With more than 35 years of experience in responding to RFPs, we have the necessary experience and resources to navigate government procurement processes. We possess the expertise and experience to assess and allocate the appropriate resources necessary for successful project completion in accordance with contractual terms.

Our clients

Our primary customers are government agencies, with the majority at the federal, provincial and state level and, to a lesser extent, some at the county and municipal level. In the United States, even when our direct customers are state governments, a significant amount of our revenue is ultimately provided by the United States Federal Government in the form of cost sharing arrangements with the states, such as is the case with Medicaid. In the year ended September 30, 2013, approximately 56% of our total revenue was derived from state government agencies whose programs received significant federal funding, 24% from foreign government agencies, 12% from U.S. federal government agencies, and 8% from other sources including local municipalities and commercial customers. We were not significantly affected by the recent shut-down of the United States Federal Government in October 2013. The nature of our programs is such that they are typically deemed essential, which means that a short-term shut-down would not be expected to cause significant disruption to our operations. However,

10

an extended delay may affect certain government programs that rely upon federal funding and may also have an effect on our cash flows from operations if payments are delayed.

For the year ended September 30, 2013, we derived approximately 14% of our consolidated revenue from contracts with the State of Texas, 12% of our consolidated revenue from the United States Federal Government and 12% of our consolidated revenue from the Commonwealth of Australia. Revenue from Texas and the United States Federal Government was principally in our Health Services Segment; revenue from Australia was exclusively within our Human Services Segment.

We typically contract with government clients under four primary contract types: performance based, fixed-price, cost-plus, and time and materials. For the year ended September 30, 2013, 48% of our contracts were performance based, 29% were fixed-price, 20% were cost plus and 3% were time and materials.

Generally, the relationships with our clients are long-term, multi-year contracts, subject to option years and periodic rebids. See the "Backlog" section below for more details.

Competition

The market for providing our services to government agencies is competitive and subject to rapid change. However, given the specialized nature of our services and the programs we serve, market entry can be difficult for new or inexperienced firms. The complex nature of competitive bidding and required investment in subject-matter expertise, repeatable processes and support infrastructure creates barriers to entry for potential new competitors unfamiliar with the nature of government procurement.

Our primary competitors in the Health Services Segment market in the United States are Affiliated Computer Services, a Xerox Company; Electronic Data Systems, an HP Company; and specialized private service providers. Our primary competitors in the Human Services Segment market include Serco, Atos Origin, other specialized consulting companies and non-profit organizations.

Legislative initiatives

We actively monitor legislative initiatives and respond to opportunities as they develop. Over the past several years, legislative initiatives created new growth opportunities and potential markets for us. Legislation passed in all the geographies in which we operate has significant public policy implications for all levels of government and presents viable business opportunities in the health and human services arena. We are well-positioned to meet the operations program management and consulting needs resulting from that legislation and subsequent regulatory and program implementation efforts.

Some recent legislative initiatives that have created new growth opportunities for us in the government market include the following:

ACA. In March 2010, the United States enacted comprehensive health care reform, known as the Affordable Care Act (ACA). This law is designed to expand access to health coverage to more than 30 million Americans, protects consumer rights, control health care costs, and improves the overall health care delivery system over the course of the next four years and beyond. On June 28, 2012, the Supreme Court of the United States upheld ACA while allowing states to opt out of the previously mandated Medicaid expansion. The law presents several business opportunities for us to offer our expertise in the administration of public programs, including:

11

insurance exchanges offer new avenues to enrollment; states may also see an increase in participation rates among Medicaid-eligible individuals;

Numerous legislative attempts to repeal the ACA have failed thus preserving ACA and the related business opportunities. In addition, the President has repeatedly stated that he would veto such legislation. As a continued sign of support, the administration transferred monies from other programs to support the implementation of the ACA. Further, the federal exchange was designed to be a temporary function thereby providing additional time for the implementation of state based insurance exchanges. Additional monies may become available to promote state based insurance exchanges.

Shift to Medicaid Managed Care. As Medicaid programs become larger, more complex and costly, states look to new models. Estimates from the Centers for Medicare and Medicaid Services (CMS) indicate that although the fee-for-service system covers less than half of the total Medicaid population, it accounts for more than 80% of all Medicaid spending. In response, several states have initiatives to reduce the current costs of Medicaid by moving different populations of beneficiaries from fixed-fee-for-service models to managed care, which represents new growth opportunities for us.

CHIPRA. CHIPRA was signed into law on February 2, 2009, extending the previous SCHIP program. As part of the ACA, CHIP has been extended through 2019 and funding has been extended through 2015, which is two additional years beyond the original CHIPRA Act. By expanding state options to find and enroll eligible children through "express lane eligibility" and "auto enrollment," CHIPRA has presented us with an opportunity to expand our partnerships with states for the administration of CHIP programs. The advent of state and federal exchanges at the beginning of 2014 will increase participation of eligible children in CHIP.

Work Programme in the United Kingdom. The Work Programme, part of the Coalition government's debt reduction measures, is a government-sponsored welfare-to-work model that consolidates several existing employment programs into a single comprehensive back-to-work program in an effort to achieve higher quality, longer-term and sustainable employment outcomes for job seekers in the United Kingdom. The Work Programme presented new opportunities for MAXIMUS and we have been delivering employment services throughout Thames Valley, Hampshire and the Isle of Wight and West London since June 2011.

12

Employment Program of British Columbia. In 2009, the Province of British Columbia (BC) and the Government of Canada signed a Labour Market Development Agreement that delegates responsibility for delivery of employment and training programs from the federal to the provincial level. In response, the new Employment Program of BC was created to provide all British Columbians eligible for work a single point of entry to employment and labor market services. This program represents a shift in policy to a consolidation and integration of programs into a "one-stop" and "employment first" model with required contracted services that are responsive, inclusive, accessible and client-centered. This program presented an opportunity for us to expand its workforce services offerings to new jurisdictions.

Backlog

At September 30, 2013, we estimate that we had approximately $3.4 billion of revenue in backlog. Backlog represents an estimate of the remaining future revenue from existing signed contracts and revenue from contracts that have been awarded, but not yet signed. Our backlog estimate includes revenue expected under the current terms of executed contracts and revenue from contracts in which the scope and duration of the services required are not definite but estimable (such as performance-based contracts). Our backlog estimate does not assume any contract renewals.

Increases in backlog result from the awarding of new contracts or the extension or renewal of existing contracts and option periods. Reductions come from fulfilling contracts and early termination of contracts. Increases and decreases can follow from changes in management's estimates, particularly for performance-related contracts.

Our contracts typically contain provisions permitting government customers to terminate the contract on short notice, with or without cause. The backlog associated with our performance-based contracts is an estimate based upon management's experience of case loads and similar transaction volume from which actual results may vary.

We believe that period-to-period backlog comparisons are difficult and may not necessarily accurately reflect future revenue we may receive. The actual timing of revenue receipts, if any, on projects included in backlog could change for any of the aforementioned reasons. The dollar amount by segment of our backlog as of September 30, 2013 and 2012 was as follows:

| |

As of September 30, |

||||||

|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | |||||

| |

(In millions) |

||||||

Health Services |

$ | 2,379 | 1,412 | ||||

Human Services |

1,021 | 1,488 | |||||

Total |

$ | 3,400 | 2,900 | ||||

Our BPS businesses typically involve contracts covering a number of years. Once contracts are signed, they typically take three to six months to begin generating revenue. At September 30, 2013, the average weighted life of these contracts was in excess of 5.5 years, including options. Although the exercise of options is uncertain, we believe the incumbent contractor enjoys significant advantages. The longevity of these contracts assists management in predicting revenues, operating income and cash flows. We expect approximately 43% of the backlog balance to be realized as revenue in fiscal 2014 and, with the inclusion of anticipated option period renewals, to represent approximately 95% of current estimated 2014 revenues.

Employees

As of September 30, 2013, we had approximately 12,000 employees, consisting of 9,000 employees in the Health Services Segment, 2,800 employees in the Human Services Segment and 200 corporate

13

administrative employees. Our success depends in large part on attracting, retaining and motivating talented, innovative, experienced and educated professionals at all levels.

As of September 30, 2013, 450 of our employees in Canada were covered under three different collective bargaining agreements, each of which has different components and requirements. There are 438 employees covered by two collective bargaining agreements with the British Columbia Government and Services Employees' Union and 12 employees covered by a collective bargaining agreement with the Professional Employees Association. These collective bargaining agreements expire in 2015.

As of September 30, 2013, 938 of our employees in Australia were covered under a Collective Agreement, which is similar in form to a collective bargaining agreement. The Collective Agreement is renewed annually.

None of our other employees are covered under any such agreement. We consider our relations with our employees to be good.

Other information

MAXIMUS is a Virginia Corporation, founded in 1975.

Our principal executive offices are located at 1891 Metro Center Drive, Reston, Virginia, 20190. Our telephone number is 703-251-8500.

Our Internet address is http://www.maximus.com. We make our website information available for information purposes only. It should not be relied upon for investment purposes, nor is it incorporated by reference into this Form 10-K.

We make our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and the proxy statement for our annual shareholders' meeting, as well as any amendments to those reports, available free of charge through our website as soon as reasonably practical after we file that material with, or furnish it to, the SEC. Our SEC filings may be accessed through the Investor Relations page of our website. These materials, as well as similar materials for other SEC registrants, may be obtained directly from the SEC through their website at http://www.sec.gov. This information may also be read and copied at the SEC's Public Reference Room at 100 F Street NE, Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

Glossary

Key terms included in this section of our Annual Report on Form 10-K include the following:

ACA—The Affordable Care Act, also known as Health Reform or Health Care Reform

CHIP—Children's Health Insurance Program

CHIPRA—Children's Health Insurance Program Reauthorization Act

Our operations are subject to many risks that could adversely affect our future financial condition and performance and, therefore, the market value of our securities. See Exhibit 99.1 of this Annual Report on Form 10-K under the caption "Special Considerations and Risk Factors" for information on risks and uncertainties that could affect our future financial condition and performance. The information in Exhibit 99.1 is incorporated by reference into this Item 1A.

14

We own a 60,000 square foot office building in Reston, Virginia. We also lease offices for operations, management and administrative functions in connection with the performance of our services. At September 30, 2013, we leased 114 offices in the United States totaling approximately 2.0 million square feet. In four countries outside the United States, we leased 174 offices containing approximately 0.6 million square feet. The lease terms vary from month-to-month to ten-year leases and are generally at market rates. In the event that a property is used for our services in the United States, we typically negotiate clauses to allow termination of the lease if the service contract is terminated by our customer. Such clauses are not standard in overseas leases.

We believe that our properties are maintained in good operating condition and are suitable and adequate for our purposes.

The Company is involved in various legal proceedings, including contract and employment claims, in the ordinary course of its business. The matters reported on below involve significant pending or potential claims against us.

In March 2009, a state Medicaid agency asserted a claim against MAXIMUS, related to a discontinued business line, in the amount of $2.3 million in connection with a contract MAXIMUS had through February 1, 2009 to provide Medicaid administrative claiming services to school districts in the state. MAXIMUS entered into separate agreements with the school districts under which MAXIMUS helped the districts prepare and submit claims to the state Medicaid agency which, in turn, submitted claims for reimbursement to the United States Federal Government. No legal action has been initiated. The state has asserted that its agreement with MAXIMUS requires the Company to reimburse the state for the amounts owed to the Federal Government. However, the Company's agreements with the school districts require them to reimburse MAXIMUS for such payments and therefore MAXIMUS believes the school districts are responsible for any amounts disallowed by the state Medicaid agency or the Federal Government. Accordingly, the Company believes its exposure in this matter is limited to its fees associated with this work and that the school districts will be responsible for the remainder. MAXIMUS has exited the federal health care claiming business and no longer provides the services at issue in this matter.

In 2008 MAXIMUS sold the SchoolMAX student information system business line as part of the divestiture of the MAXIMUS Education Systems division. In 2012, a school district ("District") which was a SchoolMAX client filed a formal arbitration notice alleging that MAXIMUS and the buyer failed to (i) use best practices in developing the software and (ii) deliver and test product releases as required by the contract. The District contended that those failures resulted in damages of at least $10 million. In December 2012, the arbitration panel denied the District's claims in their entirety. Costs related to the arbitration proceeding have been included within discontinued operations. The District subsequently filed a motion to vacate the decision of the arbitration panel which was denied by the court in July 2013. The District has appealed that ruling. Separately, in late 2012, the District asserted that MAXIMUS had defrauded the District in 2007 or 2008 by misrepresenting its intentions regarding the sale of the Education Systems division. That allegation was not part of the arbitration, and no formal claim or lawsuit has been filed. The company believes it has a number of defenses to that allegation and would contest it vigorously if it were asserted.

ITEM 4. Mine Safety Disclosures

Not applicable

15

ITEM 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock trades on the New York Stock Exchange under the symbol "MMS." The following table sets forth, for the fiscal periods indicated, the range of high and low sales prices for our common stock and the cash dividends per share declared on the common stock. All common stock and per share amounts have been adjusted for the stock split.

| |

Price Range | |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

High | Low | Dividends | |||||||

Year Ended September 30, 2013: |

||||||||||

First Quarter |

$ | 32.58 | $ | 27.20 | $ | 0.045 | ||||

Second Quarter |

40.50 | 31.76 | 0.045 | |||||||

Third Quarter |

40.69 | 35.32 | 0.045 | |||||||

Fourth Quarter |

45.35 | 34.65 | 0.045 | |||||||

Year Ended September 30, 2012: |

||||||||||

First Quarter |

$ | 21.37 | $ | 16.74 | $ | 0.045 | ||||

Second Quarter |

23.40 | 20.13 | 0.045 | |||||||

Third Quarter |

25.97 | 19.97 | 0.045 | |||||||

Fourth Quarter |

30.03 | 24.24 | 0.045 | |||||||

As of October 31, 2013, there were 63 holders of record of our outstanding common stock. The number of holders of record is not representative of the number of beneficial owners due to the fact that many shares are held by depositories, brokers, or nominees. We estimate there are approximately 22,600 beneficial owners of our common stock.

We expect to continue our policy of paying regular cash dividends, although there is no assurance as to future dividends. Future cash dividends, if any, will be paid at the discretion of our Board of Directors and will depend, among other things, upon our future operations and earnings, capital requirements and surplus, general financial condition, contractual restrictions and other factors our Board of Directors may deem relevant.

As partial consideration for the acquisition of Health Management Limited (HML) on July 1, 2013, we issued 202,972 unregistered shares of our common stock to the former owners of HML. The recipients have agreed to hold these shares for a period of at least two years. The shares were issued pursuant to Section 4(a)(2) of the Securities Act and Regulation S promulgated under the Securities Act.

16

The following table sets forth information regarding repurchases of common stock that we made during the three months ended September 30, 2013:

Period

|

Total Number of Shares Purchased |

Average Price Paid per Share |

Total Number of Shares Purchased as Part of Publicly Announced Plans(1) |

Approximate Dollar Value of Shares that May Yet Be Purchased Under the Plan (in thousands) |

|||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Jul. 1, 2013 - Jul. 31, 2013 |

4,000 | $ | 34.95 | 4,000 | $ | 102,177 | |||||||

Aug. 1, 2013 - Aug. 31, 2013 |

138,100 | 37.61 | 138,100 | $ | 97,093 | ||||||||

Sep. 1, 2013 - Sep. 30, 2013 |

3,500 | 38.86 | 3,500 | $ | 97,065 | ||||||||

Total |

145,600 | $ | 37.56 | 145,600 | |||||||||

17

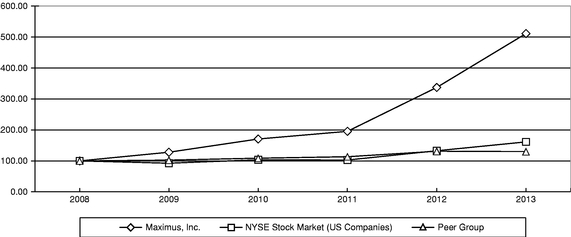

The following graph compares the cumulative total shareholder return on our common stock for the five-year period from September 30, 2008 to September 30, 2013, with the cumulative total return for the NYSE Stock Market (U.S. Companies) Index and a peer group comprising Accenture, CGI, Hewlett Packard, IBM and Xerox. The peer group companies represent a mix of information technology, BPS and management consultancy businesses and reflect a cross section of businesses against whom the Company competes for business and executive talent. The peer group is weighted by market capitalization. This graph assumes the investment of $100 on September 30, 2008 in our common stock, the NYSE Stock Market (U.S. Companies) Index, and our peer group and assumes dividends are reinvested.

Comparison of 5 Year Cumulative Total Return

Assumes Initial Investment of $100

September 2013

Comparison of Five—Year Cumulative Total Returns

Performance Graph for

MAXIMUS, INC.

Notes:

18

ITEM 6. Selected Financial Data.

We have derived the selected consolidated financial data presented below, as adjusted for discontinued operations, from our consolidated financial statements and the related notes. The revenue and operating results related to the acquisition of companies using the purchase accounting method are included from the respective acquisition dates. The selected financial data should be read in conjunction with "Management's Discussion and Analysis of Financial Condition and Results of Operations" included as Item 7 of this Annual Report on Form 10-K and with the Consolidated Financial Statements and related Notes included as Item 8 of this Annual Report on Form 10-K. The historical results set forth in this Item 6 are not necessarily indicative of the results of operations to be expected in the future. All common stock and per share amounts have been adjusted for the stock split.

| |

Year Ended September 30, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||

| |

(In thousands, except per share data) |

|||||||||||||||

Statement of operations data: |

||||||||||||||||

Revenue |

$ | 1,331,279 | $ | 1,050,145 | $ | 929,633 | $ | 831,749 | $ | 720,108 | ||||||

Acquisition-related expenses(1) |

2,168 | 2,876 | — | 254 | — | |||||||||||

Legal and settlement expense (recovery), net(2) |

(202 | ) | 90 | (808 | ) | (5,605 | ) | (4,271 | ) | |||||||

Operating income from continuing operations |

186,208 | 127,575 | 122,401 | 107,406 | 88,589 | |||||||||||

Income from continuing operations |

117,125 | 76,099 | 82,142 | 69,397 | 53,841 | |||||||||||

Income (loss) from discontinued operations(3) |

(394 | ) | 34 | (974 | ) | 1,012 | (7,301 | ) | ||||||||

Net income |

$ | 116,731 | $ | 76,133 | $ | 81,168 | $ | 70,409 | $ | 46,540 | ||||||

Basic earnings per share: |

||||||||||||||||

Income from continuing operations |

$ | 1.72 | $ | 1.12 | $ | 1.19 | $ | 1.00 | $ | 0.77 | ||||||

Income (loss) from discontinued operations |

(0.01 | ) | — | (0.01 | ) | 0.01 | (0.11 | ) | ||||||||

Basic earnings per share |

$ | 1.71 | $ | 1.12 | $ | 1.18 | $ | 1.01 | $ | 0.66 | ||||||

Diluted earnings per share: |

||||||||||||||||

Income from continuing operations |

$ | 1.68 | $ | 1.09 | $ | 1.16 | $ | 0.97 | $ | 0.75 | ||||||

Income (loss) from discontinued operations |

(0.01 | ) | — | (0.02 | ) | 0.01 | (0.10 | ) | ||||||||

Diluted earnings per share |

$ | 1.67 | $ | 1.09 | $ | 1.14 | $ | 0.98 | $ | 0.65 | ||||||

Weighted average shares outstanding: |

||||||||||||||||

Basic |

68,165 | 67,734 | 68,834 | 69,653 | 70,282 | |||||||||||

Diluted |

69,893 | 69,611 | 71,062 | 71,860 | 71,545 | |||||||||||

Cash dividends per share of common stock |

$ | 0.18 | $ | 0.18 | $ | 0.15 | $ | 0.12 | $ | 0.12 | ||||||

| |

At September 30, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | 2011 | 2010 | 2009 | |||||||||||

| |

(In thousands) |

|||||||||||||||

Balance Sheet Data: |

||||||||||||||||

Cash and cash equivalents |

$ | 125,617 | $ | 189,312 | $ | 172,950 | $ | 155,321 | $ | 87,815 | ||||||

Working capital |

227,292 | 258,606 | 227,383 | 191,461 | 164,646 | |||||||||||

Total assets |

857,978 | 695,293 | 565,279 | 527,741 | 433,234 | |||||||||||

Long-term debt |

1,489 | 1,736 | 1,696 | 1,411 | — | |||||||||||

Total shareholders' equity |

529,508 | 451,106 | 374,457 | 338,789 | 297,128 | |||||||||||

19

During the year ended September 30, 2010, the Company sold its Enterprise Resource Planning (ERP) division. The operating results of that division are shown as discontinued operations for all periods presented. The Company recorded an additional loss on the sale of the ERP division in the year ended September 30, 2011 as the final sales price was resolved. During the year ended September 30, 2013, the Company incurred additional costs related to legal matters pertaining to discontinued operations and also received funds related to the sale of a business in fiscal year 2008.

20

ITEM 7. Management's Discussion and Analysis of Financial Condition and Results of Operation.

The following discussion and analysis of financial condition and results of operations is provided to enhance the understanding of, and should be read in conjunction with, our Consolidated Financial Statements and the related Notes.

Business overview

We provide business process services (BPS) to government health and human services agencies under our mission of Helping Government Serve the People.® Our business is focused almost exclusively on administering government-sponsored programs such as Medicaid, CHIP, health care reform, welfare-to-work, Medicare, child support and other government programs. We are one of the largest pure-play health and human services administrative providers to governments in the United States, Australia, Canada, the United Kingdom and Saudi Arabia. We use our deep domain expertise, repeatable processes and technology solutions to help government agencies run efficient, cost-effective programs and to improve program accountability and outcomes, while enhancing the quality of services provided to program beneficiaries.

During the past five years, the Company has focused on its core health and human services businesses. Prior to this point, a number of non-core businesses were divested or discontinued while operations were expanded in the United States and internationally through a combination of organic growth and the acquisition of companies with complementary capabilities. We believe that this focus, balanced by a risk-management structure, has enabled the Company to attain profitable growth in recent years.

The Company believes that a combination of its record of results, robust financial performance and global experience makes it well-positioned to capitalize on opportunities in its existing markets and elsewhere. Both within the United States and internationally, governments are being challenged by factors that increase social burdens, including ageing populations and demands for health care reform, offset by reduced funds with which to deal with these demands. We believe that these trends will provide a demand for services that can be met by companies such as MAXIMUS.

Acquisitions

On July 1, 2013, the Company acquired Health Management Limited (HML), a leading provider of independent health assessments within the United Kingdom. MAXIMUS acquired HML in order to expand the Company's independent medical assessment business and to strengthen the presence of the Company's Health Services Segment in the United Kingdom. HML provided $14.1 million of revenue and $0.5 million of operating income during the fourth fiscal quarter of fiscal year 2013.

On April 30, 2012, the Company acquired Policy Studies, Inc. (PSI). PSI supports government clients in the administration of a number of health and human services programs exclusively within the United States. MAXIMUS acquired PSI, among other reasons, to strengthen its leadership in the administration of public health and human services programs. The acquired assets and business have been integrated into the Company's Health Services and Human Services Segments.

In assessing the performance of our business, we believe that it is helpful to our investors to show organic revenue growth, which represents the increase in revenue from contracts excluding those provided by our acquired businesses. Organic growth is a non-GAAP number that we believe provides a useful basis for assessing the performance of the business excluding the results of PSI and HML. In order to calculate organic growth, we remove the revenue from the acquired businesses from all periods being compared. Organic growth is not meant to be used in isolation, nor as an alternative to revenue growth as a measure of performance.

21

Financial overview

The Company has experienced strong year-over-year growth in both revenue and operating profit across both segments. There are a number of drivers of this growth.

The Company continues to see opportunities to further expand the business. In particular, the implementation of the Affordable Care Act (ACA) and Medicaid expansion in the United States has provided opportunities for MAXIMUS related to the federal and state-based health insurance exchanges. MAXIMUS estimates that ACA has added more than $150 million in new annual contract revenue for the Company from the operation of customer contact centers for five states, the District of Columbia and the United States Federal Government. In addition, MAXIMUS is providing eligibility appeals services for the federal exchange and expertise and experience to other states in their preparations for the implementation of ACA.

Although the Company's operations have expanded, cash flows from operations have been constrained through the additional requirements for working capital necessitated by the Company's growth, as well as increases in the time taken by our customers to pay us. The Company's free cash flow, which includes cash outflows related to capital expenditures, has also been tempered by the need to invest in the necessary infrastructure primarily associated with new contract awards, particularly in the United States. Overall, the Company's cash balance has declined by $63.7 million during fiscal 2013, which includes a cash payment of $71.4 million related to the acquisition of HML.

Sales pipeline at September 30, 2013 was $2.4 billion, compared to $2.6 billion at September 30, 2012. At the start of the current year, the Company had a significant number of new contracts in start-up and these converted opportunities were the principal driver behind the current fiscal year's growth in revenue. The sales pipeline only reflects opportunities where the request for proposal (RFP) is expected to be released within the next six months. Under most circumstances, contract opportunities that are carried within the pipeline reflect the base contract value and do not include future option periods. Option periods are typically reported in the pipeline six months before they are eligible to be exercised. For contracts with the United States Federal Government, it is common to see a single year base contract with multiple options, whereas state, local and international contracts typically have longer base periods. Our assessment of pipeline reflects only opportunities that the Company is pursuing or planning to pursue and should not be considered as indicative of guaranteed future revenues.

International businesses

The Company operates in international locations and, accordingly, transacts business in currencies other than the United States Dollar, principally the Australian Dollar, the Canadian Dollar, the British Pound and the Saudi Arabian Riyal. During the year ended September 30, 2013, the Company earned approximately 25% of revenues and operating income from foreign subsidiaries. At September 30,

22

2013, approximately 34% of the Company's assets are held by foreign subsidiaries. International business exposes the Company to certain risks.

The Company's revenues, profits and asset balances, including cash balances, are affected by fluctuations in the currencies noted above. When the United States Dollar is strengthening, as it was during fiscal year 2013, our international operations will contribute less revenue and profit than would have been the case had the currencies remained consistent. In assessing the performance of our business, we believe that it is helpful to our investors to show constant currency revenue growth, which represents the increase in revenue from contracts excluding the effects of year-over-year currency fluctuations. Constant currency growth is a non-GAAP number that we believe provides a useful basis for assessing the performance of the business excluding the unpredictable effects of foreign exchange movements. In order to calculate constant currency, we calculate revenue for all international businesses using the exchange rates used in the prior year. Constant currency growth is not meant to be used in isolation, nor as an alternative to revenue growth as a measure of performance.

23

Summary of consolidated results

The following table sets forth, for the fiscal year ends indicated, selected statements of operations data:

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | 2011 | |||||||

| |

(dollars in thousands, except per share data) |

|||||||||

Revenue |

$ | 1,331,279 | $ | 1,050,145 | $ | 929,633 | ||||

Gross profit |

386,033 |

287,943 |

253,651 |

|||||||

Gross profit margin |

29.0 | % | 27.4 | % | 27.3 | % | ||||

Selling, general and administrative expense |

197,859 |

157,402 |

132,058 |

|||||||

Selling, general and administrative expense as a percentage of revenue |

14.9 | % | 15.0 | % | 14.2 | % | ||||

Operating income excluding acquisition-related expenses and legal and settlement expenses and recoveries |

188,174 |

130,541 |

121,593 |

|||||||

Operating income excluding legal and settlement expense as a percentage of revenue |

14.1 | % | 12.4 | % | 13.1 | % | ||||

Acquisition-related expenses |

2,168 |

2,876 |

— |

|||||||

Legal and settlement expense (recovery) |

(202 | ) | 90 | (808 | ) | |||||

Operating income from continuing operations |

186,208 |

127,575 |

122,401 |

|||||||

Operating margin from continuing operations |

14.0 | % | 12.1 | % | 13.2 | % | ||||

Interest and other income, net |

2,851 |

4,176 |

3,495 |

|||||||

Income from continuing operations before income taxes |

189,059 |

131,751 |

125,896 |

|||||||

Provision for income taxes |

71,934 | 55,652 | 43,754 | |||||||

Tax rate |

38.0 | % | 42.2 | % | 34.8 | % | ||||

Income from continuing operations, net of income taxes |

117,125 |

76,099 |

82,142 |

|||||||

Income (loss) from discontinued operations, net of income taxes |

(394 | ) | 34 | (974 | ) | |||||

Net income |

$ | 116,731 | $ | 76,133 | $ | 81,168 | ||||

Basic Earnings per share: |

||||||||||

Income from continuing operations |

$ | 1.72 | $ | 1.12 | $ | 1.19 | ||||

Income (loss) from discontinued operations |

(0.01 | ) | — | (0.01 | ) | |||||

Basic earnings per share |

$ | 1.71 | $ | 1.12 | $ | 1.18 | ||||

Diluted Earnings per share: |

||||||||||

Income from continuing operations |

$ | 1.68 | $ | 1.09 | $ | 1.16 | ||||

Income (loss) from discontinued operations |

(0.01 | ) | — | (0.02 | ) | |||||

Diluted earnings per share |

$ | 1.67 | $ | 1.09 | $ | 1.14 | ||||

The Company's common stock was split two-for-one during the 2013 fiscal year. All results presented in these financial statements have been adjusted for this stock split.

The following provides an overview of the significant elements of our Consolidated Statements of Operations. As our business segments have different factors driving revenue growth and profitability, the sections that follow cover these segments in greater detail.

24

Fiscal year 2013 compared to fiscal year 2012

Revenue increased 26.8% to $1,331.3 million. On a constant currency basis, growth would have been 27.5%. Organic growth was 19.4%. Much of the growth came from our Health Services Segment, driven by new work, the expansion of existing contracts and the acquisitions of PSI and HML.

Gross profit increased 34.1% to $386.0 million, representing a profit margin of 29.0% compared to 27.4% in the prior year. Gross profit margins within the Health Services Segment was driven principally by the accretive nature of the higher volumes in our federal Medicare appeals business. Gross profit margins declined within our Human Services Segment, driven in part by additional costs within our Australian business.

Selling, general and administrative expense (SG&A) consists of costs related to general management, marketing and administration. These costs include salaries, benefits, bid and proposal efforts, travel, recruiting, continuing education, employee training, non-chargeable labor costs, facilities costs, printing, reproduction, communications, equipment depreciation, intangible amortization and legal expenses incurred in the ordinary course of business. Our SG&A as a percentage of revenue has remained broadly consistent between fiscal year 2013 and 2012.

Operating income from continuing operations increased 46.0% to $186.2 million for the year ended September 30, 2013, compared to the prior year. Excluding the acquisition-related expenses and legal and settlement expense, growth would have been 44.1%. This growth was driven by the acquisitions of PSI and HML, new work in our Health Services Segment and $10.9 million of income related to a terminated contract.

Interest and other income declined due to decreases in our international cash balances, which generated the majority of our interest income. These funds were used to acquire HML.

Our tax rate for fiscal year 2013 was 38.0%, compared to 42.2% in 2012. The prior year tax rate includes a charge of $2.7 million to correct an error from prior years, without which the rate would have been 40.3%. During fiscal year 2013, the Company received the benefit of increased profits in locations with lower tax rates than the United States, particularly in the United Kingdom, where the ramp up of the UK contract and the acquisition of HML resulted in profits taxed at lower rates. We anticipate that our tax rate will decline slightly during fiscal year 2014, primarily driven by anticipated profit outlook by jurisdiction.

Fiscal year 2012 compared to fiscal year 2011

Revenue increased 13.0% to $1,050.1 million. On a constant currency basis, growth would have been 13.2%. Organic growth was 6.5%. Organic growth was driven by the Health Services Segment, which was offset by declines in revenue from our international operations in the Human Services Segment.

Gross profit increased 13.5% to $287.9 million, representing a profit margin of 27.4% compared to 27.3% in the prior year. Although gross profit margins did not move significantly at a consolidated level, gross profit margins in the Health Services Segment declined and those in the Human Services Segment increased, as discussed in more detail below.

SG&A increased by 19.2% to $157.4 million. This increase is in excess of the increase in revenue and was caused by a number of factors including significant business development activity, including the preparation of bids and proposals, and the acquisition of PSI, which resulted in additional intangible asset amortization expense.

Operating income from continuing operations increased 4.2% to $127.6 million for the year ended September 30, 2012, compared to the prior year. Excluding the acquisition-related expenses and legal and settlement expense, growth would have been 7.4%. This growth was driven by the acquisition of

25

PSI, new work in our Health Services Segment and growth in our Human Services Segment. The sections below cover segment results in more detail.

Interest and other income increased primarily due to increases in cash balances in jurisdiction with higher interest rates than the United States. This increase in cash was driven by strong international cash flows.

Our effective tax rate for fiscal year 2012 was 42.2% compared with 34.8% in 2011. The tax charge in fiscal year 2012 included a charge of $2.7 million to correct an error from prior years, without which the rate would have been 40.3%. This increase was driven by a greater share of the Company's profits being recorded in the United States, which has a higher corporate tax rate than other jurisdictions in which the Company operates. The increase in profits in the United States was driven by organic growth; the acquisition of PSI, which conducted all of its business within the United States; and the anticipated decline in profits in the United Kingdom, which is discussed below.

Income from continuing operations, net of income taxes, declined 7.4% to $76.1 million. The benefits from the Company's organic growth and acquisitions were offset by the significantly higher tax rate.

Acquisition-related expenses and legal and settlement expenses

Acquisition-related expenses are direct costs incurred as a consequence of the acquisition of HML in 2013, PSI in 2012 and various other acquisitions that were not completed. These costs include legal fees, brokerage fees, due diligence, valuation reports, contract terminations related to redundant support services and severance.

Legal and settlement expense (recovery) consists of costs, net of reimbursed insurance claims, related to significant legal settlements and non-routine legal matters, including future probable legal costs estimated to be incurred in connection with those matters. Legal expenses incurred in the ordinary course of business are included in selling, general and administrative expense. Legal and settlement expenses (recoveries) are summarized below (in thousands):

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | 2011 | |||||||

Insurance recoveries |

$ | (390 | ) | $ | (1,180 | ) | $ | — | ||

Employee lawsuit |

— | 600 | — | |||||||

Client indemnification |

— | 490 | — | |||||||

Other |

188 | 180 | (808 | ) | ||||||

Legal and settlement expense (recovery) |

$ | (202 | ) | $ | 90 | $ | (808 | ) | ||

During fiscal year 2012, the Company agreed to settle a lawsuit brought by a former employee for $0.6 million and agreed to pay $0.5 million relating to client indemnification of funds misappropriated by a former employee. During fiscal year 2013, the Company's insurance provider reimbursed the Company for part of the latter claim.

The insurance recovery in fiscal year 2012 relates to a litigation settlement in fiscal year 2008.

During the 2011 fiscal year, the Company reversed a legal expense previously recognized in fiscal year 2010 for a matter that concluded without liability to the Company.

We discuss operating income from continuing operations excluding acquisition-related expenses and legal and settlement expenses and recoveries. Operating income excluding acquisition-related expenses and legal and settlement expenses and recoveries is a non-GAAP number. We believe that excluding acquisition-related expenses and legal and settlement expenses and recoveries provides a framework for comparing the performance of the business between periods as these charges do not

26

reflect the underlying performance of the business. This non-GAAP number should not be used in isolation, nor as an alternative to operating income as a measure of performance.

Health Services Segment

The Health Services Segment provides a variety of business process services for state, provincial and federal programs, such as ACA, Medicaid, CHIP, Medicare and the Health Insurance British Columbia Program.

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | 2011 | |||||||

| |

(dollars in thousands) |

|||||||||

Revenue |

$ | 862,879 | $ | 671,181 | $ | 565,881 | ||||

Gross profit |

248,100 | 172,456 | 147,239 | |||||||

Operating income |

129,834 | 80,619 | 74,715 | |||||||

Gross profit margin |

28.8 |

% |

25.7 |

% |

26.0 |

% |

||||

Operating profit margin |

15.0 | % | 12.0 | % | 13.2 | % | ||||

Fiscal year 2013 versus fiscal year 2012

Revenue increased by 28.6% to $862.9 million. Growth was not significantly affected by year-over-year fluctuations in foreign currency exchange rates. Organic growth was 22.8%. Gross profit increased by 43.9% and operating profit increased by 61.0%, with margins increasing year-over-year.

The results for the segment were driven by:

The expansion of the gross and operating profit margins was driven principally by the accretive nature of the higher volumes in our federal Medicare business.

We expect to see growth in fiscal year 2014 through the full year benefit of our contracts associated with ACA. The Health Services Segment should also receive the benefit of a full year of HML's business. We expect lower margins in the Health Services Segment in fiscal year 2014 compared with fiscal year 2013. This is driven by an expected increase in federal cost-reimbursable contracts, which tend to have lower margins; highly accretive contract work ending; and the launch of a loss-making contract that was acquired as part of the PSI acquisition.

Fiscal year 2012 versus fiscal year 2011

Revenue increased by 18.6%, or 18.9% on a constant currency basis. Organic growth was 14.8%. Gross profit increased by 17.1% and operating profit increased by 7.9%, with margins declining year-over-year.

The results for the segment were driven by:

27

Human Services Segment

The Human Services Segment includes a variety of business process services, case management, job training and support services for programs such as welfare-to-work programs, child support, K-12 special education and other specialized consulting services.

| |

Year ended September 30, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

2013 | 2012 | 2011 | |||||||

| |

(dollars in thousands) |

|||||||||

Revenue |

$ | 468,400 | $ | 378,964 | $ | 363,752 | ||||

Gross profit |

137,933 | 115,487 | 106,412 | |||||||

Operating income |

58,091 | 49,922 | 46,822 | |||||||

Gross profit margin |

29.4 |

% |

30.5 |

% |

29.3 |

% |

||||

Operating profit margin |

12.4 | % | 13.2 | % | 12.9 | % | ||||

The results for the Human Services Segment in fiscal year 2013 were affected by a one-time benefit from the termination of a system-integration contract acquired with PSI. The termination resulted in one-time, non-cash benefits to revenue of $16.0 million and to gross and operating profit of $10.9 million. Although contract terminations for convenience do occur within our business, they are infrequent. In addition, this termination was unusual due to the significant effect of the transaction as it involved deferred revenue from the PSI acquisition and does not reflect the underlying operations of the Company. We have provided a reconciliation below showing our results excluding the effect of this contract.

| |

Results for Human Services Segment for year ended September 30, 2013 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

Revenue | Gross profit | Operating profit | |||||||

| |

(dollars in thousands) |

|||||||||

As reported |

$ | 468,400 | $ | 137,933 | $ | 58,091 | ||||

Effect of terminated contract |

(16,035 | ) | (10,900 | ) | (10,900 | ) | ||||

Results excluding the effect of the terminated contract |

452,365 | 127,033 | 47,191 | |||||||

Profit margins excluding the effect of the terminated contract. |

28.1 | % | 10.4 | % | ||||||

The numbers in the table above are non-GAAP numbers, but we believe that the presentation of these numbers provides a useful basis for assessing the performance of this segment compared to prior periods or the results of our competitors. However, these non-GAAP numbers should not be considered in isolation nor as alternatives to their GAAP equivalents as measures of performance.

Fiscal year 2013 versus fiscal year 2012

Revenue increased 23.6% to $468.4 million. On a constant currency basis, growth would have been 25.4% and organic growth was 12.8%. Gross profit increased 19.4% and operating profit increased 16.4%. Excluding the effect of the termination of the contract, revenue growth was 19.4%.

Results for the segment were driven by a number of factors:

28

We are forecasting that fiscal year 2014 will be fairly flat for revenue compared to fiscal year 2013. This assumes that growth in our international operations will be offset by a decline in the United States, largely related to the successful completion of a large, multi-year, fixed-price contract. In both fiscal years 2013 and 2012, the segment enjoyed unusual benefits from two contracts that seem unlikely to be repeated in fiscal year 2014. We believe the full year segment operating margins will be towards the lower end of our stated range of 10-15%.

Fiscal year 2012 versus fiscal year 2011

Revenue increased 4.2% to $379.0 million in fiscal year 2012 compared to fiscal year 2011. On a constant currency basis, the growth would have been 4.4%. Excluding acquisition driven growth from PSI, segment revenues would have declined 6.4%. Gross profit increased 8.5% and operating profit increased 6.6%, resulting in increases to both profit margins.

The results for the segment were driven by a number of factors.

Discontinued operations